Valuing Brand and Technology Asset Indonesia

The business environment in Indonesia has evolved significantly in the last ten years. Land, machinery, and physical infrastructure are no longer the key defining factors of the most valuable businesses in the country today. They are characterized by their brand, their technology platform, their customer relations and their intellectual property. However, the official reporting and valuation of these Indonesian financial statement assets has been uneven to date, and it introduces discrepancy between reported book value and true economic value, which influences pricing in M&A, adherence to the IFRS, tax planning, and investor decision-making.

Valuation of intangible assets in Indonesia An intangible asset is no longer a specialist niche reporting requirement, but a mainstream financial reporting requirement. In connection with PSAK 22 (Business Combinations) and PSAK 19 (Intangible Assets), the acquiring companies have to find out the fair value of all the recognisable intangible assets on the acquisition date, including brands and technology, which the target might never have formally recognised on its own books. To the financial professional, the investors and intellectual property valuation experts operating in the Indonesian market, the knowledge on the valuation of brand and technology assets is critical knowledge to them.

This guide includes the entire terrain: the major concepts and standards that are applicable in practice, modern intangible asset valuation methods, the advantages of a serious valuation, the use of such models in practice, best practices in the form of documentation and compliance, as well as the pitfalls that professional intellectual property valuation practitioners often have to maneuver through.

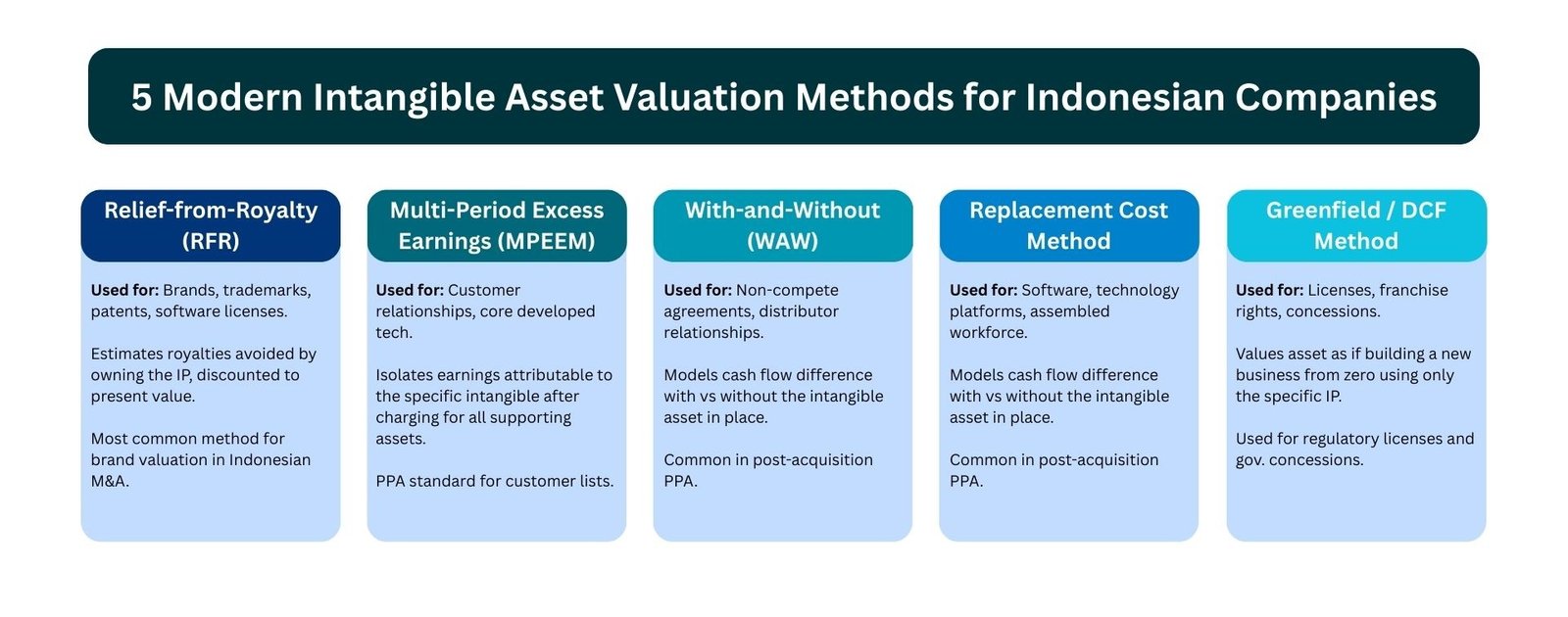

Figure 1: Five modern intangible asset valuation methods applied in Indonesian M&A and financial reporting (Valuing Brand and Technology Asset Indonesia)

Key Concepts: What Is Valuing Brand and Technology Asset Indonesia?

The valuation of intangible assets in Indonesia is the process of estimating the economic value of non-physical assets, which are mainly intellectual property (IP), brands, customer relations, software, and technology platforms, to be financial-reported, as part of a transaction advisory, as a licensing, as tax-compliant, or as part of a strategic management process.

In PSAK 19 (equivalent to IAS 38), an intangible asset has two recognition requirements, namely identifiable (separable or arising as a result of the right to a contract or under law), and probable that future economic benefits will accrue to the entity. These criteria instantly distinguish the intangibles that have to be formally valued and the goodwill, and that is, the non-identifiable, residual value, which is recorded separately under PSAK 22 and PSAK 48.

Under Indonesian M&A transactions under PSAK 22 / IFRS 3, all identifiable intangible assets are recognised at the fair value at the date of acquisition by the acquiring firm, although the target entity never did so. This is the main reason behind intangible asset valuation Indonesia demand in the corporate finance setting. The prevalent intangible assets used in the Indonesian transactions are:

- Brand names and trademarks – especially in functional and consumer-based value (FCI) product and service industries such as FMCG, food and beverage, retail, and pharmaceutical industries.

- Customer relationship and backlog of contracts- It is the current value of the revenue anticipated to be generated by current customers, less the cost of satisfying the relationship.

- Licensed technology and software platforms – such as e-commerce infrastructure, fintech credit scoring engines, logistics management systems, and digital marketplace algorithms

- Distribution and dealer networks- the benefit of existing commercial relations with distributors, retailers or agents which would be difficult and expensive to replicate.

- Franchise rights and licensing contracts – the price of contractual rights to use a brand or proprietary know-how.

- Non-competition agreements- the financial advantage of restraints denying former owners or key employees of competing.

The different types of assets need a particular valuation method, which is being tuned to the nature of the asset and the market data available in Indonesia. The five modern intangible asset valuation methods most widely applied in Indonesian practice are the Relief-from-Royalty, Multi-Period Excess Earnings, With-and-Without, Replacement Cost, and Greenfield (DCF) methods—each described in detail in Figure 1 above.

Figure 2: Key differences between brand and technology asset valuation in the Indonesian market (Valuing Brand and Technology Asset Indonesia)

Why Valuing Brand and Technology Asset Indonesia Matters in Financial and Corporate Context

The significance of stringent intangible asset valuation Indonesia spans in the fields of financial reporting, execution of M&A, tax compliance and strategic management. The answer to both questions is why it is important and to whom it is relevant would help in putting into perspective the practical course of action that must be taken to resolve it.

IFRS and PSAK Business Combinations

All business combination accounts that are less than PSAK 22 generate a liability to recognize and quantify intangible assets at fair value. With Indonesian M&A transactions which have seen an increases in both the quantity and types of deals, this is so that a substantial part of the overall value consideration paid stays in identifiable part of intangibles in lieu of undifferentiated goodwill. Firms and auditors that tackle this requirement without expert knowledge of intangible assets valuation Indonesia most of the time end up with lead-time opening balance sheets which are then contested and have to undergo costly restatements.

Once the intangibles recognised under a Purchase Price Allocation (PPA) are accurately valued and amortised over their useful lives, the balance of goodwill is reduced, the amortisation profile is more predictable and the post-acquisition income statement is a true accounting measure of the cost of the acquisition. Goodwill is overstated when intangibles are not recognized or understated, which makes the imposition of impairment testing on them inflated and provides a misleading financial statement.

Transfer Pricing and Tax Compliance

The valuation of intangible assets is one of the key components of transfer pricing regime in Indonesia. In the case where an Indonesian firm sells a brand, software platform or patented process to a related party, such as an offshore parent, subsidiary or joint venture partner, the royalty rate to be paid should be such that it returns arm length price. DJP is very vigilant about intragroup IP transactions, and royalty rates which can not be justified by separate intangible asset appraisal are at risk of being challenged, reassessed, and fined.

In the case of Indonesian firms in the digital, pharmaceutical and consumer goods industry, where the intangible assets business model entails numerous intragroup licensing agreements, the defensibility of reported values of intangible assets is not only a financial reporting issue. It is a tax risk management practice that increasingly more and more intellectual property valuation specialists are set to be employed to assist on a continuing, annual basis.

M&A Pricing and Negotiation

During the Indonesian M&A dealings, the buyer and the seller often do not agree on the value of intangible assets, especially those brands with long history and decades-long customer base. An independent intangible asset valuation Indonesia report that is credible will serve as reliable anchoring point in these negotiations and will also minimise the chances of paying too much and also the failure to realise the real IP value.

On the contrary, sellers that require pre-deal intangible asset valuations are more likely to defend their asking prices especially in those businesses in which the majority of the value is held in quantifiable IP. In the emerging digital economy of Indonesia, where technology startups and platform companies are habitually acquirer by listed conglomerates, the brand and technology assets can be the wholesale value thesis, and their separate valuation is a deal requirement and not an a posteriori compliance position.

Strategic IP Management

In addition to transactions and reporting, intangible asset valuation in Indonesia has a strategic role to play: it is one way of management to know which of the IP assets are most valuable, which need investment to maintain their existence, and which could be the target of licensing, divestment, or enforcement action. Indonesian firms that have made intensive IP valuation, and which use their valuation to make portfolio investment decisions, allocate R and M spending in a more efficient way than the ones that make decisions based on intuition.

Key Benefits of Professional Valuing Brand and Technology Asset Indonesia

A company which invests in specialised intangible asset valuation Indonesia will always reap the rewards which go far beyond the short term compliance or transaction scenario.

Factual Opening Balance Sheets During Acquisition

An open balance sheet with all intangible assets reported and their value properly determined results in a comprehensive PPA that brings about the reality of the acquisition in terms of its economic aspects. It is important in a number of ways: it makes the balance of goodwill reduce (annual impairment testing can be more easily performed), it results in a more realistic amortisation profile which reflects the economic utilisation of the value acquired, and it offers the audit committee and OJK the disclosure that is necessary under the PSAK 22 requirements.

Defensibility of Royalty Rate of Transfer Pricing

The first line of defence against DJP transfer pricing difficulties is an independently prepared intangible asset valuation with support of observable market royalty data and documented approach. When the royalty rate adopted in an intragroup licensing plan is identifiable to a particular valuation procedure and to a distinct group of readily visible market analogies, the risk of a long-term DJP challenge is significantly lessened. This advantage can substantiate the expenditure on annual IP valuation maintenance of the Indonesian groups where the intragroup licensing is a significant activity.

IPO and Capital Market Readiness

The capability to provide a well-documented intangible assets register indicating the nature of key IP company assets, their fair value and useful life is a statement of financial reporting maturity that should be very appealing to the institutional investors, underwriters and OJK reviewers. The companies that continued their annual corporate intangible asset valuation as a financial governance framework are in much better states to go through the IPO readiness process than the companies that met the requirement first time.

Dispute Support and Litigation

Where intangible assets are subject to conflict such as an infringement of the IP, shareholder claim regarding business value, damage to a licensing agreement, and so on, the demonstrative basis of legal action is an independent methodology-documented intangible asset valuation. The use of expert evidence of valuation in cases arising under the IP category is gaining momentum in the Indonesian courts and arbitral tribunals and the reliability of the evidence is determined by the methodology that is used, the independence of the expert who is preparing the evidence and the standard of the documentation.

Practical Applications: Valuing Brand and Technology Asset Indonesia Across Industries

The value of intangible assets in Indonesia is applied with a meaning difference across sectors. The cases below are the trend in the Indonesian financial advisory and transaction practice.

Case One: FMCG Brand Portfolio Valuation for a Consumer Goods Acquisition

A Indonesian diversified conglomerate purchased a local snack and beverage brand that had a good distribution coverage in Java and Kalimantan. The overall consideration of IDR 2.1 trillion involved a significant premium over the target net asset value, leading to a full blown PPA under PSAK 22. The intellectual property valuation experts engaged to lead the exercise identified four intangible assets requiring formal valuation: the primary brand trademark, two regional sub-brands, and a distributor network covering approximately 4,800 points of sale.

Relief-from-Royalty was the method used to value the primary brand. The rate of royalty, which was established to be 3.5 per cent of estimated branded revenue, was based on a survey of observable trademark licensing structures in the Indonesian FMCG market, which was complemented by regional comparable data in Malaysia and Thailand. The royalty stream was estimated during a useful distance of 15 years (terminal value was the potential of brand indefinite life), with discount rate of brand specific WACC of 13.8% of the brand risk premium over the cost of equity.

The distributor network was valued under the With-and-Without technique where it is assumed that the revenue decreases and the incremental cost a buyer would face in the estimated 18 months period taken to establish similar coverage of distribution on their own. The identified total intangibles of IDR 760 billion of all four assets was 36% of the total consideration, which significantly decreases the goodwill balance what would have been created by a less comprehensive PPA.

Case Two: Technology Platform Valuation for a Fintech Acquisition

Financial holding company listed in Jakarta bought a majority (70 percent) of a fintech lending platform and in the process paid IDR 890 billion to a business with a net balance sheet amounting to IDR 120 billion. The main source of value was the proprietary credit scoring algorithm by the platform, which was developed in four years and trained on the loan applications of about 2.3 million. One of the secondary assets was the OJK lending licence which the platform had.

The valuation specialists employed to perform the PPA used the Multi-Period Excess Earnings Method to appraise the credit scoring technology. The model separated incremental cash flows that could be specifically attributed to the technology, once mid-way charges have been made on all other supporting assets such as the workforce, physical infrastructure and customer relationships and discounted incremental cash flows to a rate that captures the specific risk of the technology such as risk of competitive disruption and algorithmic obsolescence. The useful life of the technology was fixed at five years, which depicts the pace of transformation in credit scoring technique in the digital lending market of Indonesia.

It was decided that the OJK lending licence was to be valued on a cost approach basis, which was based on the estimated regulatory capital, compliance infrastructure and time that management would need to take to acquire a similar licence in the new regulatory environment adjusted using the likelihood of success on a new application. The combined intangibles of IDR 590billion resulted in goodwill of IDR 180billion- which was the synergy value of the combination of the technology of the target with the financial distribution network already owned by the acquirer.

Case Three: Pharmaceutical Patent Portfolio Assessment

An intangible asset valuation Indonesia was commissioned by a multinational pharmaceutical company with a presence in Indonesia in connection with the review of its transfer prices in Indonesia concerning a local portfolio of local patents and trademarks. The portfolio consisted of 12 active product patent, three manufacturing process patents, and four registered trademarks of the prescription and over-the-counter product lines.

The intellectual property valuation specialists used the Relief-from-Royalty technique of the product trademarks and a mixture of Greenfield DCF technique and replacement cost approach to the process patents- the income technique was limited by the challenge in identifying cash flows due to manufacturing efficiency enhancement and not other factors. The resulting royalty rates between 1.2 percent and 4.8 percent based on product type, position in the market and life of the patent were the arm-length benchmarks needed in the intercompany licensing agreements of the company and would underpin the transfer pricing documentation submitted with the DJP.

Transfer pricing insight:

In the case of the Indonesian pharmaceutical and technology firms having intragroup IP licensing, the best single step in mitigating DJP transfer pricing audit risks is to have the most current, independent valuation of their intangible assets, (i.e., current as of the date of the annual financial statements) in order to reflect changes in revenue, market position, and remaining IP life.

Table 1: Intangible Asset Valuation Indonesia — Asset Type, Method, Useful Life, and Key Considerations (Valuing Brand and Technology Asset Indonesia)

| Intangible Asset | Primary Method | Typical Useful Life | Discount Rate Adj. | Indonesia-Specific Note |

| Brand / Trademark | Relief-from-Royalty | 10–20 yrs / Indefinite | +2–4% brand risk | Royalty 0.5-8 percent; FMCG and retail market data of Indo and SEA. |

| Customer Relationships | MPEEM | 5–12 years | +2–3% customer risk | Attrition: 10-25% p.a.; service industry more than B2B. |

| Developed Technology | MPEEM or Cost | 3–7 years | +3–5% tech risk | Critical functional obsolescence; 5yr maximum of digital assets. |

| Distribution / Dealer Network | With-and-Without | 5–10 years | +2–4% | Rebuild time 12-24 months; exclusivity has an influence on the range of values. |

| Non-Compete Agreement | With-and-Without | Contract term | Low / contract rate | 2-5 years in duration; associated with particular exit of founders/execs. |

| Franchise / License Rights | Greenfield DCF | Remaining term | +2–3% license risk | Government concessions: tenure of stay. |

| Process Patent / Trade Secret | Replacement Cost / RFR | Patent life remaining | +3–5% | DJP transfer pricing: recommended intragroup annual valuation. |

Source: Compiled from Indonesian M&A transaction practice and PSAK 19 / IAS 38 guidance.

Best Practices for Valuing Brand and Technology Asset Indonesia

- Practice An overview of practices that consistently characterize the high quality of intangible asset valuation work versus technically satisfactory work which may be commercially unsatisfactory is identified by the finance professionals, transaction advisers and intellectual property valuation experts working in Indonesia

- Choose the appropriate approach on each particular asset – resist the urge to use the same method on all intangibles in a PPA. Relief-from-Royalty technique is suitable in the case of brands and trademarks; MPEEM is suitable in the case of customer relationships and core technology; With-and-Without is better in the case of non-competes and distribution arrangements. An incorrect method gives a technically valid and economically inaccurate outcome.

- Calibrate royalty rates against visible data in the Indonesian and regional marketplace – the greatest problem in brand valuation is the choice of a royalty rate without adequate market facts. The valuation experts conducted by Intellectual property should compile a list of comparables based on noticeable licensing deals within the industry industry plus published royalty rates surveys, and explain why the central market rate had to be breached.

- Have Indonesian market inputs all the way through – discount rates ought to be constructed out of Rupiah based elements (Indonesian Government Bond yield, Indonesian equity risk premium, sector beta using IDX data). When USD-based discount rates are applied to the cash flows of the intangible assets of IDR-based assets without currency adjustments, it generates systematically low discount rates and over-stated asset values.

- Pre-coordinate with auditors – the intellectual property valuation professionals must coordinate the methodology, scope of identification of assets, and key assumptions ranges with the external auditors of the acquiring entity prior to the model of the valuation being developed. The major reason behind PPA restatement and late financial statement release in Indonesian, M and A deals is the post-fieldwork methodology disagreements.

- It should have documented visible evidence of all major assumptions – all royalty rates, attrition assumptions, contributory asset charges, and every element of the discount rate must be linked to a particular market observation, published data or documented professional judgment. It is the quality of documentation that will dictate the quality of the audit trail, not to mention the ease with which the valuation will stand the test of time.

- Have up to date transfer pricing valuations – in a company where intragroup IP licensing is used, annual renewal of the intangible asset valuation is a transfer pricing compliance obligation not an option. The transfer pricing audit programme that has been running to evolve by the DJP has been more based on IP-intensive transactions, and the valuation that is more than two years old is unlikely to meet the current arm-length documentation requirements.

Common Challenges in Valuing Brand and Technology Asset Indonesia and How to Address Them

The valuation of the intangible assets in Indonesia has certain challenges that are more acute in comparison with the more advanced valuation markets. The fact that these issues exist and the professional reactions to them exist constitutes what distinguishes the successful intellectual property valuation experts and the generalist financial advisors.

Sparse Data on Observable Royalty Rate

The Relief-from-Royalty approach entails the existence of observable royalty rate standards of similar licensing deals. Indonesia In Indonesia, publicly disclosed IP licensing agreements are fewer than in the US or European markets, so the task of the valuers is to combine the regional (ASEAN and Asia-Pacific) data with the global industry surveys (placed in RoyaltySource or ktMINE) and use their own judgment concerning the suitable adjustment of the Indonesian market context.

The answer is to construct a formal, documented analysis of comparables: to find the largest possible set of transactions in the market of royalty rates, to filter by screening factors to the closest similar transactions, and then explicitly to adjust to the factors of Indonesia that are specific, market position, economic environment, and particular competitive dynamics in the industry in question. This is more important than the falseness of precision in the end rate, as it would be done in a transparent manner.

Impairment of Technology Assets of Rapid Obsolescence

The digital and technology capabilities in Indonesia, such as credit scoring algorithms, e-commerce platforms, logistics management systems, are experiencing the rate of change that renders the traditional useful life assumptions impractical. The assumption of the seven-year useful life of a machine learning model scheduled to be retrained periodically and compete with constantly changing substitutes can be technically consistent with PSAK 19 but can be economically misguided.

The model of functional obsolescence: selected by people operating in this field, the intellectual property valuation professionals must model the functional obsolescence explicit: what is the pace at which the current technology would be defeated by existing market alternatives, even without any physical degradation. It is especially vital to the technology assets of the Indonesian fintech and e-commerce sector, wherein the competitive environment is dynamic at best and the usability of any particular technical architecture is three to five years at most.

The Spotting of Intangibles in Pre-Acquisition Due Diligence

Another problem that is common to Indonesian M&A is the inability to identify all the intangible assets in pre-acquisition due diligence, which means that the result of the PPA is technically sound but lacking economic completeness. This is usually the case where the deal team emphasized on financial due diligence at the cost of IP due diligence or where the management of the target has never carried out an official IP audit.

The answer is to put an IP identification procedure as part of the due diligence procedure and not as a post-closing PPA exercise but as a pre-signing activity. An interview, as part of the systematic IP identification, where the target management is interviewed with the review of intellectual property valuation professionals prior to finalisation of the deal structure, would have the value allocation structure known to both parties before consideration is given. This eliminates after closing conflicts over PPA findings and guarantees that earn-out arrangements, representation and warranty arrangements, and price modifying models demonstrate the real IP framework of the business under purchase.

Match Intangible Values and General Deal Pricing

In other Indonesian deals, the identified intangible asset values in a serious PPA process are larger than those that the deal team expected in the deal at the time of negotiating the price of the deal. This may cause conflict between the purchase price allocation needed to meet the financial reporting obligations and internal transaction model to support the deal economics. The valuation experts in the Intellectual Property field must acknowledge this conflict and urge the finance department to learn about the accounting reasons behind it- instead of modifying the valuation products to generate a pre-constrain finding.

PSAK 22 states that the PPA should be based on the real fair values of assets obtained rather than convenient allocation, which reduces accounting complexity. A PPA that is created due to commercial pressure (to ensure amortisation charges are low or due to inflating goodwill) is not PSAK-compliant and will be questioned by auditors. The correct action to unforeseen intangible values is to reform the post-acquisition integration plan as well as earnings model and not the valuation.

Conclusion: Making Intangible Asset Valuation a Core Capability in Indonesia (Valuing Brand and Technology Asset Indonesia)

Appreciating brand and technology assets in Indonesia is no longer a high-level specialisation that is limited to the biggest transactions and most sophisticated market players. With an increasingly IP-intensive economy (by digital transformation, brand-building investment, and deeper penetration of the Indonesian M&A market) intangible asset valuation Indonesia is turning out to be a conventional competence that needs to be cultivated and sustained by finance professionals, corporate advisers, and intellectual property valuation experts.

The essence of this guide is that intangible assets are not peripheral to the Indonesian business value they are often the centre of it. The brand value an FMCG creator established in three decades, the credit scoring system an IT team developed out of four years, the distribution channel system an association manager managed during the ten years, all these moats provide the Indonesian businesses a premium price in capital markets dealings, the licensing rights that allow sustainable intragroup revenues, and the portfolio of intellectual property that supports a high-price acquisition.

The next step in corporate financial governance in Indonesia is the recognition, measurement, and management of these assets in the same intensity as tangible property and financial instruments. The given normative modern methods of valuing intangible assets as outlines in this article: Relief-from-Royalty, MPEEM, With-and-Without, Replacement Cost, and Greenfield DCF are the means of analytical tools. The professional standard that is now demanded is to apply them properly with market inputs of Indonesia, documented assumptions, and methodology that is led by experts.

To acquire the professional competence to work in this area, it is clear to finance professionals that they should have the following practical starting points: learn how the intangible assets are disclosed in the financial reports of the IDX listed companies after major acquisitions; learn how to be fluent in the royalty rates benchmarking in at least one of the main industries in Indonesia; and learn to establish working relationships with intellectual property valuation professionals who can offer not only professional advice but also the market data that would make their intangible valuation practices in Indonesia credible, not only compliant.