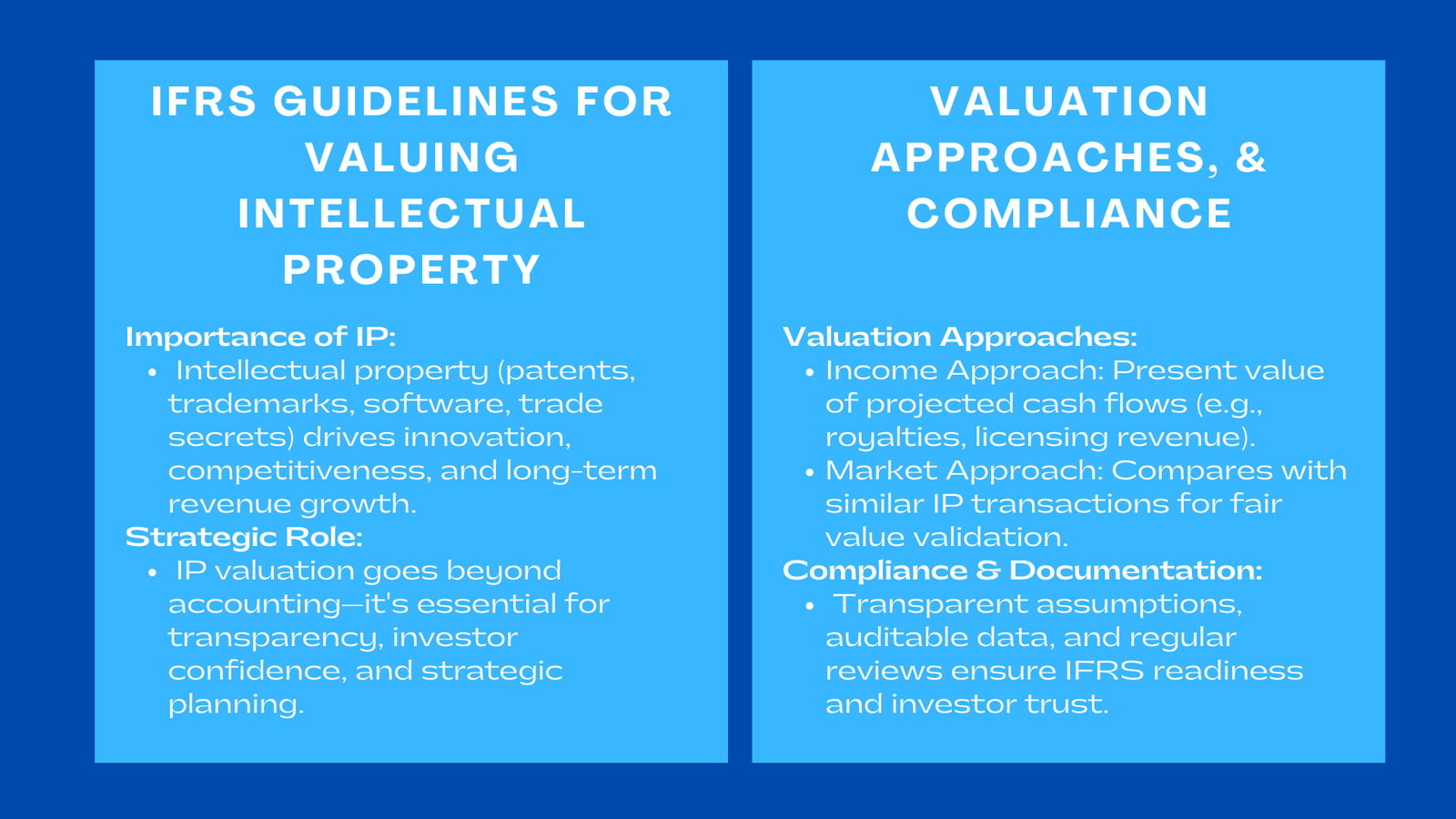

IFRS Guidelines for Valuing Intellectual Property

Intellectual property (IP) has emerged as one of the most critical intangible assets for modern organizations, playing a vital role in defining market positioning, competitive differentiation, and long-term revenue potential. In the knowledge-driven global economy, the ability of a company to innovate, protect, and strategically leverage IP determines its capacity to sustain growth, attract investors, and respond to rapidly evolving markets. IP includes patents, trademarks, copyrights, proprietary software, trade secrets, designs, and technological innovations, all of which provide the foundation for a company’s competitive advantage.

For startups and SMEs, IP often represents the core value of the business. A small technology company may have limited physical assets but possess proprietary algorithms or software that generate substantial future revenue. Similarly, creative industries rely heavily on copyrights, trademarks, and design rights to maintain brand identity and consumer loyalty. The economic contribution of IP extends beyond legal rights; it is directly linked to cash flow potential, scalability, and strategic opportunities in licensing, partnerships, and acquisitions.

Accurate valuation of IP is not merely an accounting requirement; it is a strategic imperative. Misvaluation or failure to recognize IP can distort financial reporting, mislead investors, and limit opportunities for growth. IFRS-compliant valuation ensures that IP is accurately represented on the balance sheet, enabling organizations to demonstrate transparency, governance rigor, and economic credibility. Furthermore, IP valuation accounting IFRS allows companies to integrate intangible assets into broader corporate strategy, supporting informed decision-making, effective resource allocation, and maximized enterprise value.

IFRS Recognition Criteria and Classification of Intellectual Property

Identifiability and Control Requirements

To recognize IP as an intangible asset under IFRS standards, specifically IAS 38 and IFRS 3, the asset must satisfy identifiability and control criteria. Identifiability ensures that the IP can be separated from the business, transferred, sold, licensed, or independently exploited. For instance, a patented technology can be licensed to third parties or used as a basis for joint ventures, demonstrating clear separability. Understanding these principles is also relevant when assessing how to determine net tangible asset value Singapore, as both tangible and intangible assets play critical roles in accurately reflecting a company’s overall financial position and enterprise value.

Control requires that the company has the legal or contractual rights to derive economic benefits from the IP and restrict others from using it. This may include patent ownership, licensing agreements, or exclusive distribution rights. SMEs and startups often encounter challenges in proving control, especially for internally developed software or proprietary processes. Legal safeguards, robust IP registration, and enforceable contracts are essential to demonstrate control in line with IFRS requirements.

Economic Benefit and Useful Life Considerations

IP recognition under IFRS also hinges on the expectation of future economic benefits. These benefits can arise from licensing revenue, product commercialization, market differentiation, operational efficiencies, or enhanced customer loyalty. Determining the expected benefits requires comprehensive analysis of market dynamics, competitive landscape, and potential revenue streams.

The useful life of an IP asset is equally critical. Technology-based assets such as software algorithms, pharmaceutical formulas, or industrial designs may face rapid obsolescence due to innovation, regulatory changes, or market disruption. IFRS mandates that the amortization of intangible assets aligns with their useful life, ensuring that financial statements accurately reflect the value of assets over time. Long-lived patents may require amortization over decades, while digital applications might need accelerated schedules and frequent impairment testing.

Valuation Methodologies: Income, Market, and Cost Approaches

Income Approach: Projecting Cash Flows

The Income Approach is widely considered the most robust method for valuing IP. It calculates the present value of future cash flows that the IP is expected to generate. This requires detailed revenue forecasting, including licensing fees, royalties, subscription income, and cost savings attributable to the asset. Cash flows are then discounted using risk-adjusted rates that account for market volatility, competitive risk, and economic uncertainty.

For example, a pharmaceutical company may project revenue from a patented drug based on expected sales volume, pricing strategies, market penetration, and licensing agreements. Similarly, a technology startup may value its proprietary software by estimating subscription revenue and potential enterprise contracts over its useful life. Scenario analysis is crucial to understand the range of potential outcomes, allowing management to make strategic decisions under uncertainty.

Market Approach: Comparable Transactions

The Market Approach estimates IP value by examining recent transactions involving similar intangible assets. While it can be challenging to identify exact comparables, especially for proprietary or niche innovations, this method provides a benchmark to validate Income Approach valuations.

For example, if a startup develops a blockchain-based solution, the Market Approach may analyze licensing deals, acquisitions, or investments in comparable blockchain startups to estimate a fair value range. By integrating multiple sources of market data, companies can improve the reliability of their valuations, supporting negotiations in M&A, fundraising, or licensing agreements.

Cost Approach: Replacement and Reproduction Costs

The Cost Approach considers the amount required to recreate the IP, including R&D expenditures, legal fees, patent registration costs, and administrative overhead. This method is particularly relevant for internally developed assets lacking observable market data. It establishes a minimum value by reflecting the resources required to reproduce or replace the asset.

For instance, a software company may calculate the development costs of a proprietary platform, including salaries, technology infrastructure, testing, and legal expenses, to determine its replacement value. The Cost Approach also aids in internal decision-making, resource allocation, and budgeting, providing insight into the economic investment required to maintain IP assets.

Amortization, Useful Life, and Impairment

Dynamic Lifespan of Intellectual Property

The useful life of IP is inherently variable, influenced by technological advancement, market adoption, and regulatory changes. A software application may become obsolete within a few years, whereas a patent for a chemical compound may maintain value for decades. Companies must adopt flexible amortization schedules that reflect realistic economic lifespan and support IFRS-compliant financial reporting.

Impairment Testing and Documentation

Regular impairment testing ensures that the carrying value of IP does not exceed its recoverable amount. This requires monitoring revenue forecasts, market trends, competitive pressures, and technological changes. Documentation of assumptions—such as discount rates, growth projections, and market dynamics—is essential to support auditability and transparency.

For example, a startup that develops mobile applications must monitor app downloads, user engagement, and competitor apps to determine whether the IP retains its value or requires impairment recognition. Clear documentation not only satisfies regulatory requirements but also enhances stakeholder confidence and demonstrates corporate governance rigor.

Challenges in Data Reliability and Documentation

Cross-Functional Data Integration

IP valuation requires robust, auditable data from multiple departments, including finance, legal, operations, R&D, and marketing. Historical costs, licensing agreements, projected revenues, market research, and competitive intelligence must be consolidated to produce a reliable and comprehensive valuation.

Startups and SMEs often face challenges due to limited systems for capturing and organizing data. Developing centralized data management frameworks and robust recordkeeping processes ensures transparency and facilitates accurate valuation, even as IP portfolios expand or evolve.

Ensuring Compliance and Audit Readiness

Documenting valuation methodologies, assumptions, and data sources is essential for IFRS compliance and audit readiness. Transparent reporting builds credibility with regulators, investors, and potential partners. Companies that can demonstrate structured IP management are better positioned to attract investment, secure partnerships, and negotiate licensing deals effectively.

Compliance with IFRS also reduces the risk of legal challenges or regulatory penalties. Regular internal reviews and cross-functional collaboration ensure that IP valuation remains aligned with corporate strategy and audit standards.

Strategic Implications of IP Valuation

Leveraging IP for Business Growth

IP valuation provides a roadmap for strategic growth. Accurately valuing IP supports licensing agreements, M&A negotiations, investor fundraising, and market expansion strategies. For instance, a startup with a patented technology can attract venture capital investment or negotiate favorable joint ventures based on a robust, IFRS-compliant IP valuation.

Enhancing Brand and IP Compliance

Aligning IP valuation with IFRS strengthens overall brand and IP compliance. Transparent reporting, structured revaluation, and proactive governance demonstrate corporate responsibility and reassure stakeholders that IP is a core asset.

Well-managed IP valuation also enhances brand equity. A company recognized for valuing its innovations signals reliability, foresight, and operational maturity, reinforcing investor confidence and market trust. Strategic integration of IP valuation into corporate planning ensures that intangible assets directly contribute to enterprise value, operational efficiency, and competitive differentiation.

Supporting Decision-Making and Risk Management

Accurate IP valuation informs strategic decisions, including product development, licensing, partnerships, and international expansion. It also facilitates risk management by identifying assets susceptible to technological obsolescence, market volatility, or regulatory challenges. Organizations that continuously monitor, revalue, and integrate IP insights into decision-making maintain a proactive approach to asset management, mitigating potential financial and operational risks.

Conclusion to IFRS Guidelines for Valuing Intellectual Property

Intellectual property is no longer just a legal safeguard or an accounting footnote—it is a strategic asset capable of shaping corporate growth, competitive positioning, and investor perception. IFRS provides a rigorous framework for IP valuation, ensuring that intangible assets are accurately recognized, measured, and reported in financial statements.

Organizations that adhere to Brand and IP Compliance reap multiple benefits. They not only comply with regulatory requirements but also gain actionable insights that support licensing, investment, mergers, acquisitions, and strategic partnerships. By applying Income, Market, and Cost Approaches, companies can triangulate fair value estimates, enhance credibility, and align asset valuation with economic reality.

Regular amortization schedules, impairment testing, and revaluation ensure that IP valuations remain dynamic, responsive to technological advancements, and aligned with market realities. Startups and SMEs benefit particularly from structured IP valuation, as it provides a tangible measure of intangible assets, attracts investors, and supports strategic business planning.

Beyond compliance, IFRS-aligned IP valuation strengthens brand and IP governance. Transparent documentation, auditable methodologies, and periodic reassessment demonstrate corporate responsibility and operational maturity. Stakeholders gain confidence that intangible assets are managed effectively, strategic decisions are data-driven, and enterprise value reflects both tangible and intangible contributions.

In conclusion, integrating IFRS-compliant IP valuation into business strategy transforms intellectual property from a conceptual asset into a measurable growth driver. It enhances transparency, supports investor relations, informs strategic planning, and safeguards enterprise value. Organizations that adopt disciplined IP management practices are better equipped to innovate, compete, and achieve sustainable long-term success in today’s knowledge-driven and rapidly evolving global economy. IP valuation is no longer optional—it is a strategic imperative that bridges the gap between intangible innovation and tangible business growth.