How Singapore Companies Value

Intangible Assets for IFRS 3 PPA

Introduction to Singapore Value Intangible Assets

The importance of Intangible Valuation in PPA

In cases where a Singapore firm buys out another business, the amount that it pays to the company is seldom equal to the value of the knowable assets. They are equipment, inventory and property, but in the case of most modern businesses, in particular those based on technology, financial services, and professional markets, the premium inherent in the purchase price is nearly entirely of the intangible variety: brand awareness, clientele, proprietary platform and rights of contract.

That is the reason why the intangible asset valuation PPA takes centre stage in acquisition accounting. In the acquisition approach required in PPA IFRS 3 Singapore, the acquirer is required to recognize the total consideration paid to all identifiable assets and liabilities and to recognize them at their fair values at the acquisition-date. The intangibles which were never reflected on the own balance sheet of the acquiree because most internally generated intangibles are not capitalised under IAS 38 have to be realised, recognised and measured afresh.

The economic implications are very high. Recognised intangibles are amortised, and earnings after acquisition are lowered in a regular and foreseeable manner. Goodwill the remaining, when identifiable net assets are determined, is not amortised but it is also liable to impairment testing each year, which can present significant and unpredictable charges in case of acquisition performance failure. The accuracy of the PPA valuation requirements exercise thus directly influences the manner in which the acquired business is represented to the investors, regulators and lenders years after closing of the deal.

Connection of IFRS 3 and Financial Reporting Results

The manner in which business combination intangible exercise is established under the IFRS 3 has a long term spill over effects on the financial statements of an acquirer. When a PPA is properly made to recognise and measure customer relationship and brand equity and technology assets, amortisation charges will be higher but the amount of goodwill will be lower and more defendable. A PPA that concentrates all excess consideration in a higher amount in goodwill will artificially boost near-term earnings per share but it will introduce a narrowly-focussed impairment risk, and can be a subject of regulatory review.

In the case of Singapore-based firms and multinationals with subsidiaries in Singapore, there is a lot at stake. All the interests of the quality of disclosures of the acquisition accounting are in the Singapore Exchange (SGX), the Accounting and Corporate Regulatory Authority (ACRA), and the Monetary Authority of Singapore (MAS). The balance sheets of companies with goodwill are under more and more scrutiny by investors and analysts. And auditors – who are mandated to assess the completeness and reasonableness of the PPA – are increasingly subjecting fair value intangible assets of acquisition accounting to increasingly greater rigour.

Overview Purchase Price Allocation

IFRS 3 Principles

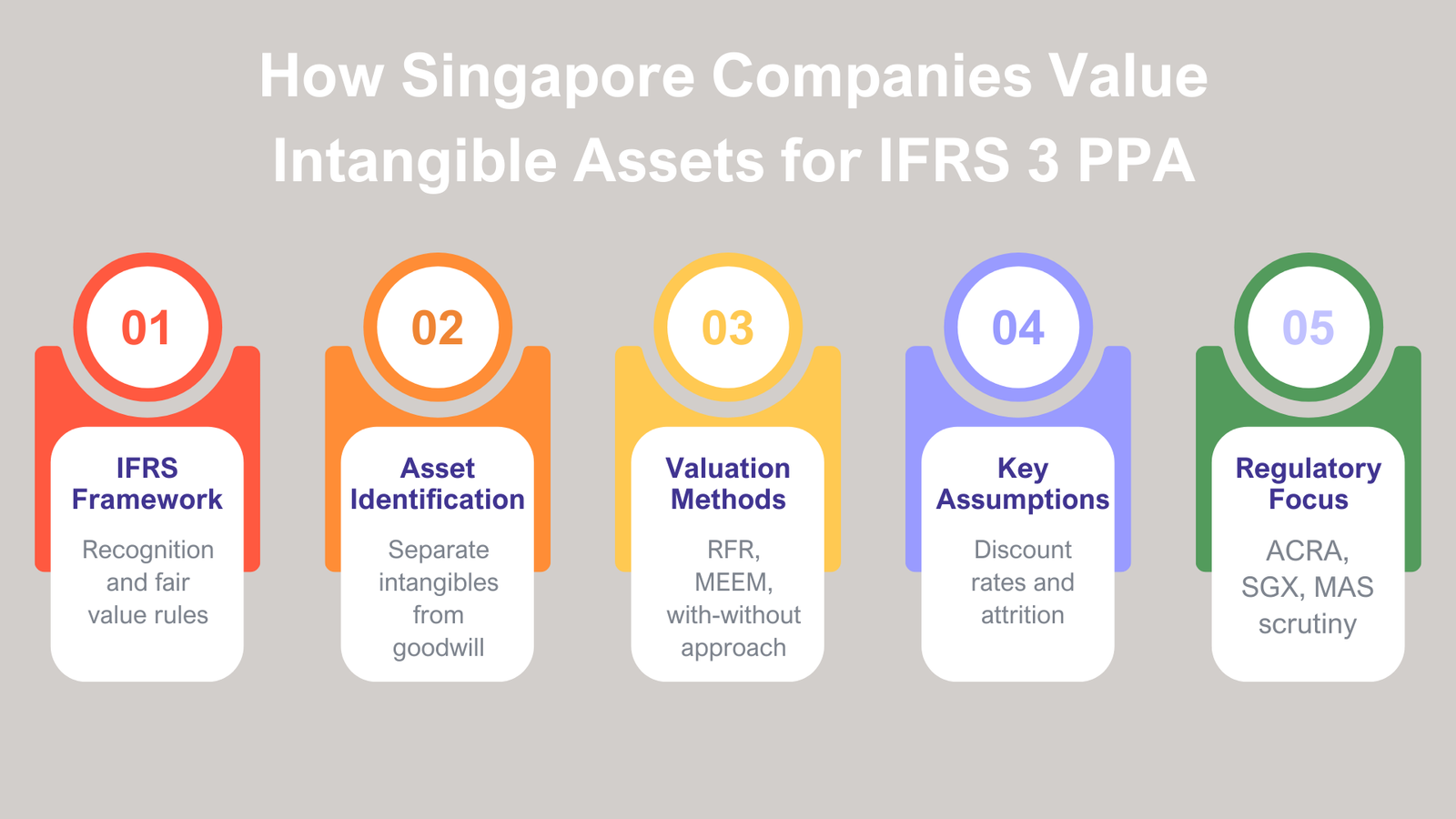

Any exercise on PPA IFRS 3 Singapore is based on the basis of acquisition method that IFRS 3 Business Combinations requires all business combinations to adopt. The acquisition technique needs the acquirer to:

- Who is the acquirer – a person who gains control over the acquiree.

- Identify the date of acquisition — the date of taking control.

- Identify and record all identifiable assets, liabilities, and non-controlling interests at the fair value of their acquisition-date.

- Goodwill, or gain due to a sale by a bargain, should also be recognised and measured as the remaining amount.

The starting point is total consideration transferred – i.e. cash paid, shares issue, contingent consideration at fair value, and previously held interests at acquisition-date fair value. The transaction costs are not taken into consideration and charged as incurred. The period of measurement (the period in which the provisional values can be adjusted retrospectively as new information is available) should not be more than 12 months since the date of acquisition.

Investigations of Allocation Intangible Valuation Role

The identification and valuation of intangible assets is generally the most complicated part of a PPA IFRS 3 Singapore exercise. Tangible assets, as compared to their intangible counterparts, can be relatively easy to measure either through the market or the cost method, but fair value intangible assets and need specialised income-based approaches, sector-specific assumptions as well as detailed financial modelling.

Practical implications of intangible asset valuation PPA can be explained by the fact that purchase price in the majority of modern deals consists of different parts. Financial services, technology and consumer acquisitions of brand, all of which are common place in Singapore, often comprise of 40-75% intangible assets of total consideration. Without an appropriate identification and measuring of these assets, the whole PPA is skewed as the goodwill is overstated, amortisation is undervalued, and the nature of the acquired value is misrepresented.

Detecting Intangible Asset of PPA

The initial step of the PPA IFRS 3 Singapore exercise in any business combination is the identification of business combination intangible assets. Under IFRS 3, intangible assets should be recognised other than goodwill should they be identifiable (satisfy either contractual-legal requirement (generated by legal or contractual rights) or the separability requirement (capable of separation and sale, licensing or transfer). The categories that are most widespread in Singapore acquisitions are as follows.

Customer Assets

The most important value fair intangibles in intangible acquisitions of Singapore service sector include customer relationships. They include the economic worth of a prevailing customer base – the anticipation of recurring revenues and the escape of the cost of acquiring customers. Contractual customer relationships (retainers, multi-year contracts of providing services, or licensed product subscription) and non-contractual relationships (loyal retail customers or advisory clients who have no formal contracts) can both be potentially recognised under IFRS 3.

In non-contractual relationships, the separability criterion is satisfied since it is a common type of transaction in financial services, insurance, healthcare and professional services industries to buy and sell customer lists and books of business. The important variables that cause customer relationship value include: the revenue per customer, the gross margins that can be attributed to relationship, the projected rate of annual attrition (churn), and cost and time that is needed to replace the departing customers.

Other intangibles that are related to the customers are customer order backlog (contractual orders at the time of acquisition that are yet to be delivered) and customer contracts. Backlog Backlog is the intangible that is usually short-lived and amortised over the period of fulfilment of orders but may be a material item to project based or long cycle business.

Brand and Marketing Assets

The intangible value of business combination core is Brand equity both in consumer-facing and B2B business. Legally registered (as trademarks) trade names, logos, and brand identities directly satisfy the contractual-legal requirement. Commercially recognisable brands that are not registered can satisfy the separability criterion when it is possible to observe similar transactions in regard to brand licensing and sales.

Brand recognition in the Singapore market is a premium priced and customer loyalizing factor in the competitive retail and financial services and F&B markets. Valuation PPA of intangible assets The relief-from-royalty approach is the main one employed in the brand-related PPA to transform brand-attribution revenues into a capitalised stream of royalty savings.

Other intangibles that are based on marketing and are not considered as trade names include internet domain names, social media handles and proprietary marketing databases. Although each may have a small value on its own, they are commonly held as a subset of a larger brand intangible, or as a part of a composite trade name intangible.

Technology and Intellectual Property

In the case of technology firms, fintechs and companies that have developed technology as their core business, the strongest intangible business combination is often developed technology. The types of technology that are acquired encompass core platform code, algorithms, machine learning models, databases and proprietary tools. Under the IFRS 3, acquired technology has to be identified and measured as separate fair value intangible assets amounts even when the acquirer never capitalised the development costs in the IAS 38.

Under the contractual-legal criterion, it is possible to distinguish intellectual property assets such as patents, utility model, registered design and trade secret. Their fair value is a stream of royalty that they might have commanded in the event of licensing, or the revenues that they earn out of exclusive use. The economic life of technology and IP assets are usually lower than the brand or customer relationship, which denotes the rate of technological advancement in the rapidly changing digital economy of Singapore.

Contract and licensing assets 342.599

Favourable contracts – contracts in which the acquired entity is inclined to bear conditions that are more favourable than the existing market rates – are fair value intangible assets in PPA valuation criteria. These are below-market leases (that create an asset based on avoided rental premium), preferred supplier, exclusive distribution, and above-market customer rights.

The regulatory licences are especially applicable in Singapore where the Monetary Authority of Singapore (MAS) grants Capital Markets Services (CMS) licences, Financial Adviser (FA) licences and other licences, which are rare, precious, and can be transferred. A separate intangible under the requirements of PPA IFRS 3 Singapore 2003 is a licence that is transferable and has got an independent market value.

Covenant contracts, in which the vendor or key employees are prohibited to compete with the organisation after the deal, such as non-compete agreements, are contractual-legal and separately recognised. Their value is limited by the restriction period and harm that would be detrimental to the competition that would be in case of their absence.

Selection of Method of Valuation of PPA

Brand Relief-royalty

The usual valuation method of intangible assets in valuation PPA practice is the relief-from-royalty (RFR) method of brand valuation. Its theoretical foundation is beautiful: the owner of a brand is not obliged to pay royalties to a third party licensor. The brand fair value is the capitalised value of those shunned royalty payments. This approach is highly agreeable to auditors, regulators and tax authorities since it pegs brand value to that which is evident in the market-observable information- actual royalty rates of similar licensing deals.

The procedure will follow 5 steps:

- Determine the royalty rate base: Revenue accruing to the brand, less revenue accruing to non-branded.

- Choose royalty rate to be supported: Based on third-party royalty databases (RoyaltyRange, ktMINE, or Consor) or top-down analysis of brand contribution to profitability.

- Project brand revenues: Reflecting market growth assumptions, project brand revenues are a product of the remainder of the economic life of the brand.

- Tax-effect the royalty payments: Royalties are usually deductible on the tax bill; the after-tax economic advantage to the brand-owner.

- Discount to present value: Calculation of the discount using the risk-adjusted rate of the specific risk profile of a brand.

Customer Relationships MEEM

Multi-Period Excess Earnings Method (MEEM) is a major approach of valuing customer relationships in the practice of PPA valuation requirement. The present value of the after-tax cash flows that are due to the customer relationship after subtracting fair returns on all other assets tangible and intangible assets that generate such cash flows, are estimated by MEEM. These deductions are referred to as contributory asset charges (CACs) and it is a technically challenging yet vital aspect of the method.

When it is under MEEM the customer relationship value is addicted by:

- Revenue forecast per customer group: Disaggregated where possible by life, location or product line.

- Attrition rate: Percentage (by revenue) of customers that are likely to give up the service each year – the most sensitive input to the analysis.

- Attributable operating margins: The profit margin that can be attributed to the revenues which have been generated due to the existing customer body, post operating costs but pre-CACs.

- Contribution asset charges: Fair returns on working capital, fixed assets, brand, technology and workforce which subsidize the customer relationship.

- Discount rate: This is usually the WACC plus an asset-specific risk-premium, since the relationships with customers are nevertheless riskier than those with the business as a whole.

- Other Dynamic Income-Based Methods.

Other than RFR and MEEM, other income-based methods are used in intangible asset valuation PPA.

With-and-Without Method: Comparison of present value of cash flows with the one in place and without. Regulatory licences, favourable contracts and non-compete covenants are the most frequently used. The value is the present value of the cash flow difference between the two scenarios probability-weighted of the possibility of competitive harm.

Excess Earnings Method (single period): This is a simplified form of MEEM applicable where the asset yields uniform (as opposed to multi-period declining) earnings. Suitable to stable and repeated customer deals or perpetual licence.

Greenfield Method: The value of an operating licence or franchise right is estimated using a model of the cash flow that it would take to develop a similar business without the licence (that is, fund it without the licence). Of special importance to the financial licence issued by MAS in Singapore.

Market and Cost Methods of PPA

The market approach determines fair value of intangible assets by referring to the prices paid in observed comparable assets of other intangible assets. It is best applied in cases where there is adequate similar transaction information available, e.g. royalty rates of similar brand licence, or multiples of transactions based on similar customer books of business. The market approach as a primary methodology is not commonly used in PPA IFRS 3 Singapore practice, but often plays a corroborative role to check the conclusion of incomes approach because direct type of comparable data in the market is rare.

Cost approach measures fair value as the cost of reproduction or replacement of the intangible with the consideration of the functional, technological and economic obsolescence. It is best used in internally developed technology, assembled databases, and proprietary processes that have little information on income and market data. In PPA valuation requirements, cost approach is common with developed software, CRM databases and training materials especially in small Singapore SME acquisitions where revenue history is scarce.

Calibration of input which is Singapore specific

Local availability of Market Data

The local data sources and the international benchmarks should be combined to calibrate the PPA inputs of the valuation of intangible assets to the Singapore market conditions. Singapore is a regional financial centre, so that some of the market information, especially of listed companies transactions, property and financial services, is comparatively available. Nonetheless, in the case of privately-traded companies, niche markets, and specialised intangibles, lack of data is a factual constraint.

Local data sources of PPA IFRS 3 Singapore SGX-listed company transaction announcement (which reveals the deal multiples and minimal disclosure of intangibles), financial sector statistics released by the MAS, market reports released by industry association, and subscription-based global databases such as Bloomberg, Capital IQ and BvD Orbis and there is Singapore filtering. In the case of royalty rate benchmarking, international databases like RoyaltyRange and ktMINE are usually utilized with amendments to suit the Singapore market conditions.

Discount rates, the country risk, and industry risk

The most influential input is the discount rate that will be used in the analysis of fair value intangible assets. In the case of Singapore entities, discount rate construction would commonly be done under the build-up or CAPM approach that includes:

Risk-free rate: This is based on Singapore Government Securities (SGS) yields, which indicate that Singapore has the AAA-equivalent credit rating.

Equity risk premium (ERP): The ERP in Singapore is based on the country risk premium dataset by Damodaran or on local market information; it is not quite high in comparison with regional ones, which indicates the macroeconomic stability in the country.

Beta: Industry-specific beta, which should have been estimated over a portfolio of similar listed companies in the Singapore market and the region, is unlevered and re-levered based on the capital structure of the target.

Size premium: Smaller or private companies use the size premium to indicate that due to illiquidity risk and limited diversification, they involve higher risk.

Specific risk premium: Specific uncertainty of deal, risk of management concentration, risk of customer concentration and other idiosyncratic risk.

In case of individual intangible assets, a further asset premium is added to the WACC due to the fact that various intangibles have a variation of risk profiles. The discount rates on customer relationships (which are prone to loss) are usually higher than those of brands (which are less volatile). This asset specific premium model has to balance out to the WACC by a Weighted Average Return on Assets (WARA) analysis.

Economic Growth Market Multiples

The assumptions of revenue growth that are included in the requirement of PPA valuation should show the perceptions of the market-participants regarding the economic direction of Singapore. The growth due to the emerging economies such as Singapore is assessed by the expansion rates of its sectors (especially financial services and technological and healthcare), consumer spending patterns and this is all used in the growth assumptions of the intangible asset valuation PPA models.

Singapore is an open, trade based economy, and thus the entities level projections are greatly affected by the macroeconomic conditions all over the world, such as interest rate cycles, the growth trend of China and the demand trend in the region. The 20242025 valuations, with high interest rates and regional growth returning to normal are expected to necessitate more conservative growth assumptions than the low-rate high-growth 20192021 prepared valuations.

The market multiples EBITDA, revenue, or typical book value multiples based on similar public companies trading or M&A deals are employed both as a sanity check on conclusions about using the income approach and are the principal inputs in some applications of the market approach. In the case of Singapore-specific industries, the comparables, regional (Hong Kong, ASEAN-listed and ASEAN), and global ones are usually combined to obtain strong benchmark ranges.

Challenges Singapore Specific deals

Family-Owned Business Valuations

Much of the SME market in Singapore is owned by the family – as in, businesses that have ownership, management, and most important customer relationships vested in the hands of a single or two people. This structure poses unique PPA valuation and issues. The relationships with customers that the founder considers to be personal and effective may not satisfy the separability requirement of being recognized separately as a part of business combination intangible assets; rather, they can rightly be included in the goodwill.

The most important analysis question would be whether the customer relationships would withstand a hypothetical ownership shift – in other words, whether a market participant that purchases the business would have been able to expect to maintain the relationships without the personal efforts of the original owner. In the case of retention, which is at all viable (due to the institutionalisation of relationships by the business brand, systems, and personnel), a customer relationship intangible is suitable. In situations where the only way to retain is the continued existence of the founder, the value is in goodwill and the PPA should reflect the same.

There are also data problems with family-owned business PPA. The estimates of revenue can be informal, financial accounts might not be as detailed as they would be with MEEM analysis, and customer loss data can never have been recorded. Professional judgement is needed to make plausible projections using limited evidence on the part of the practitioners.

Cross-Border Components

There are numerous Singapore acquisitions that contain cross-border components, that is, targets whose operations are located in Indonesia, Malaysia, Vietnam, or other ASEAN jurisdictions. In the case of cross-border transactions the PPA IFRS 3 Singapore exercise should take into account not only the requirements of Singapore SFRS(I) but possibly that PSAK (Indonesian standards), MPERS (Malaysian standards) or other local framework in which subsidiary accounts are needed.

The presence of currency translation, country specific risk premium and the information that is available in the local market all contribute to the complexity of fair value intangible assets measurement in intercountry transactions. A brand present in both Singapore and Indonesia might require being appreciated in terms of royalty rate standards, growth trends, and rivalry in both markets. The customer relationships in Vietnam can have a higher probability of attrition and short economic life than customer relationships in the Singapore market that is more stable.

Regulatory Scrutiny and Disclosures

The Singaporean regulatory environment lays a lot of stress on the standards of disclosure of material acquisitions. The listing regulations of SGX demand that listed issuers disclose the transaction details, independent valuation (in case of interested-party or very substantial transaction), post-completion financial disclosure. The interest in the quality of acquisition accounting by ACRA has been heightened and now auditors are more obliged to determine whether all business combination intangible identification has been performed.

Additional disclosure and approval rules can be in place in the case of financial sector acquisitions that are governed by MAS. This is due to the fact that a combination of SGX, ACRA and MAS management would put Singapore acquisition accounting under a multi-layered regulatory prism whereby PPA valuation requirements are not only technically correct but also well-presented in financial statement notes and other supporting documentation.

Financial Statements Compliance and Disclosure

Disclosures that are required under IFRS 3

The IFRS3 has heavy disclosure requirements that are aimed to facilitate the financial statement users to assess the nature and financial implications of business combinations. The main disclosures that should be made in PPA IFRS 3 Singapore are:

The date of acquisition or purchase, the name and description of the acquiree and the percentage of the voting interests purchased.

The main motives of the business combination and how the acquirer took the control of the business.

The fair values of all major classes of consideration transferred, the fair value of which is all contingent consideration, the date of which is the acquisition date.

The acquisition-date fair values of the total assets acquired and total liabilities assumed, and distinct line items respectively on the fair values of major classes of intangible assets recognised.

The level of goodwill and what constitutes that goodwill such as the qualitative description of synergies, assembled labour force and other non-identifiable drivers of value.

Any benefit of a bargain purchase, why the transaction brought a benefit, and how it was determined.

In case the initial accounting is not complete at reporting date, the provisional amounts and a statement explaining why the accounting is not complete is to be provided.

In the case of material acquisitions, IAS 36 will compel disclosure of the manner in which goodwill has been apportioned to cash generating units (CGUs) and the main assumptions, on which the annual impairment tests (during which management estimates the cash flows) are based, including growth rates, discount rates, and the period of time against which management anticipates such cash flows.

Audit Requirement and Regulatory Requirement: ACRA, SGX, MAS

According to Singapore Standards on Auditing (SSAs), Singapore auditors reviewing the valuation of intangible assets of PPA are obligated to consider whether the client is complying with IFRS 3. In the case of material intangibles, it is normally through the incorporation of the valuation experts of the audit firm to audit the PPA methodology, assumptions and decisions of the acquirer.

ACRA has indicated, via its Practice Monitoring Programme, and by means of its cellular advice to the general, that acquisition accounting, and the identification and measurement of business combination intangible assets in particular, represents a focus audit quality area. Any company that has used simplified methods in the PPA process (including attributing all excess consideration to goodwill) which is not able to demonstrate an adequate process of identifying the intangibles may have an audit qualification risk.

Under its continuing disclosure oversight, SGX Regulation focuses on the acquisition accounting disclosure of listed issuers. The issuers whose goodwill disclosure lack granularity or that their documentation of PPA valuation requirements is inadequate, may be asked to provide query letters that may call further clarification or restatement. Prudential evaluations of financial strength and capital adequacy are also concerned with acquisition accounting quality in the case of MAS-regulated entities.

Practical PPA Example

The scenario is the acquisition of a Singapore HR Technology Platform

Trying to demonstrate the principles of intangible asset valuation PPA in quantitative terms, we can use the following hypothetical situation:

| Intangible Asset | Valuation Method | Key Assumptions | Fair Value (S$M) | Useful Life |

| Customer relationships | MEEM | 10% attrition; 8-yr horizon; 24% EBITDA margin; WACC+3% | S$14.2M | 8 years |

| Developed technology platform | Relief-from-Royalty | 5% royalty rate; 6-yr life; WACC+2% | S$8.5M | 6 years |

| Trade name “TechHR” | Relief-from-Royalty | 1.5% royalty rate; 12-yr life; WACC+1% | S$3.8M | 12 years |

| Non-compete (founders, 3 yrs) | With-and-Without | 15% revenue-at-risk; 3-yr horizon; probability-weighted | S$1.6M | 3 years |

| Favourable client contracts | Income approach (direct) | Below-market SaaS pricing on 4 enterprise contracts | S$0.9M | 2 years |

| Total Identified Intangibles | S$29.0M | Weighted avg: 7.2 yrs | ||

| Residual Goodwill | Synergies, cross-sell, assembled workforce | S$4.5M | Indefinite (impairment tested) |

The Impact of the Intangible Fair Values on the PPA Result

The financial ramification of this intangible asset valuation PPA exercise is radical. The acquirer would have recognized S$33.5 million (88% of excess consideration) of goodwill without recognizing and valuing the intangibles. Goodwill is also cut down to S$4.5 million – only 12% of excess consideration following the PPA. The balance of S29 million is recognised as identifiable fair value intangible assets and amortised over its respective useful life.

The post-acquisition effect on income statement is as below:

| Intangible Asset | Fair Value | Useful Life | Annual Amortisation |

| Customer relationships | S$14.2M | 8 years | S$1.78M p.a. |

| Technology platform | S$8.5M | 6 years | S$1.42M p.a. |

| Trade name | S$3.8M | 12 years | S$0.32M p.a. |

| Non-compete | S$1.6M | 3 years | S$0.53M p.a. |

| Favourable contracts | S$0.9M | 2 years | S$0.45M p.a. |

| Total annual amortisation | S$29.0M | S$4.50M p.a. |

The post-acquisition reported earnings are decreased by the annual amortisation charge of S$4.5 million. Nevertheless, it gives a much clearer picture of the consumption of the acquired assets over time – and a goodwill balance of S$4.5 million is much more justifiable and less prone to impairments compared to the S$33.5 million a simple exercise of PPA IFRS Singapore would have produced.

Best Practices of PPA Intangible Valuation

Use of Independent Experts

It is advisable to seek the services of an experienced independent valuation specialist in intangible asset valuation PPA in any transaction in which intangible assets are significant. Three different benefits are associated with independent specialists; the technical knowledge of income-based appraisal techniques; the objectivity which minimizes management bias in setting projections; and the credibility that makes the audit review process easier.

In the case of Singapore, the qualified specialists tend to possess a qualification of Chartered Valuer and Appraiser (CVA), CFA charter holder, CA (Singapore), or RICS or ASA membership. The specialist must be involved promptly preferably before or after closing of the deal so that the PPA is ready within the measurement period and provisional values are available in case of interim reporting.

Independent PPA valuation requirement support cost is generally small compared to overall deal consideration – normally 0.10.5 percent of transaction value in SME transactions – and is a reasonable investment in financial statement quality, audit quality and regulatory supportability.

Sensitivity Analysis and Scenario

Not only a base-case valuation is needed to come up with robust fair value intangible assets conclusions but also systematic sensitivity and scenario analysis. Analysis of sensitivity- An analysis of sensitivities of the key uncertainties of intangible values can be explained with the help of sensitivity analysis in which one of these assumptions is varied and kept constant at the same time. Scenario analysis – exploration of evaluation under consistent bundles of alternative assumptions (e.g. a downside revenue scenario or an accelerated attrition scenario) is a more comprehensive way of seeing the range of values.

Sensitivity analysis to test valuations in customer relationships must at least test: +2 percentage points attrition rate, +1 percentage point discount rate and +10 percent revenue projections. In valuations of brands, the variables are royalty rate sensitivity (±0.51) and revenue growth sensitivity. Such reporting in the PPA report is analytical rigour and prepares the acquirer to questions of the auditor challenge.

Audit Support and Documentation

PPA IFRS 3 Singapore standard of documentation should enable full review by the auditors without further clarification. The typical PPA valuation report has:

Outline of the executive summary of the scope of the PPA, decisions and major conclusions about the methodologies.

Information about the business and the deal, deal structure and deal consideration.

Upon identification of intangible assets: Analysis of how every asset was evaluated in respect to the IFRS 3 recognition criteria should be documented.

Rational behind the choice of valuation methodology of each asset, and providing a rationale of why that method is the best.

Extensive model documentation: financial projections, source of assumptions, sensitivity tables and WARA reconciliation.

Summary allocation table reconcile total consideration to all fair-valued assets, liabilities and residual goodwill.

The preparation of documentation must be done at the same time as the valuation, and not prepared retrospectively. Auditors are vigilant of post-event rationalisation and will demand to see that they were made earlier than the eventual finding on valuation.

Conclusion

Why Intangible Robust Valuation Saves Stakeholders

The standard of intangible asset valuation PPA in Singapore acquisition accounting is not a technical nicety – it is a basic safeguard to all the interests of the financial reporting ecosystem. To acquirers, the compliance with strict PPA valuation requirements can guarantee that the post-acquisition financial statements are based on the economic reality, which can be used as a good benchmark to evaluate the performance and allocate capital, as well as monitor impairments.

Detailed disclosures of fair value, intangible assets in detail would give the investors and analysts the transparency they require to access the quality of the acquisitions, amortisation profiles, and make independent opinion of the risk of goodwill. In the case of the lenders and creditors, a properly documented PPA contributes to credit evaluation and covenant supervision. And to regulators to ACRA, SGX and MAS high-quality business combination intangible accounting is an indicator that the company financial reporting is of standard expected of a well-managed, transparent business.

On the other hand, poor PPA in the form of undifferentiated goodwill balance that hides actual acquisition exposes the company to audit risk and regulatory examinations and possible restatements. The reputational cost of bad acquisition accounting in a market where investor trust is obtained only with difficulty and lost easily may be much greater than the reputational cost of doing it right.

Capital Markets Strategic Advantages

To Singapore companies that operate in capital markets, be it as acquirers trying to explain deal rationale to their stakeholders, as acquiring companies trying to prepare their selling process, or as listed companies trying to maintain their investor relations, the quality of PPA IFRS 3 Singapore has strategic, non-compliant meaning. When a firm is able to undertake stringent PPAs consistently, it serves to show that the management team of the firm knows what it is purchasing, at what cost and even the returns that will be obtained on the assets purchased. This is an indication of analytical discipline and financial governance credibility to the institutional investors.

The quality of acquisition accounting is becoming a differentiator in the competitive capital environment in Singapore where companies in the market compete not only with other local companies but also with listed companies in the Asia-Pacific. Companies whose PPA are clean and well documented have better scrutiny of their investors, and have less scrutiny by regulators, and they develop a record of successful acquisition execution that helps in future deal-making.

Finally, the requirement of PPA valuation under PPA IFRS 3 Singapore is a mere statement of an undisguised yet tacit fact, which is that the value of anything that the company purchases must be disclosed in the same rigour and transparency as any other item in its financial statements. The high standard of the capital market in Singapore is a legal requirement as well as an indicator of management quality in the sophisticated capital market of Singapore.