Certified IFRS Brand Reporting Compliance

Ensuring Compliance with IFRS in Brand Reporting: Difficulties in Realizing Achievement of IFRS Compliance

Introduction to Certified IFRS Brand Reporting Compliance

Transparency and consistency of reporting is very important in the present globalized financial setting as it helps preserve the confidence of investors and regulatory trust. This transparency includes brand reporting which entails the recognition, measurement and disclosures of brand related intangible assets. Nevertheless, adherence to International Financial Reporting Standards (IFRS) in brand valuation and reporting is one of the most difficult issues of corporate financial management.

Although the frameworks and guidelines are well established, most organizations continue to have difficulties in putting the IFRS requirements into compliance processes that are applicable in practice. These challenges have been caused by the complexity of intangible assets valuation, differences in interpretation, data constraints and changed standards. This paper discusses the important issues that firms encounter in obtaining the compliance of IFRS brand valuation especially considering the fact that Singapore has stringent corporate governance framework in which brand reporting standards Singapore require a combination of both accuracy and accountability.

1. Contextual IFRS Compliance in Brand Reporting.

1.1 The IFRS role in the disclosure of intangible assets.

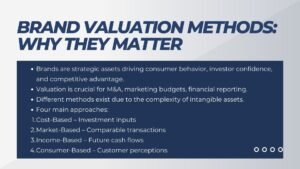

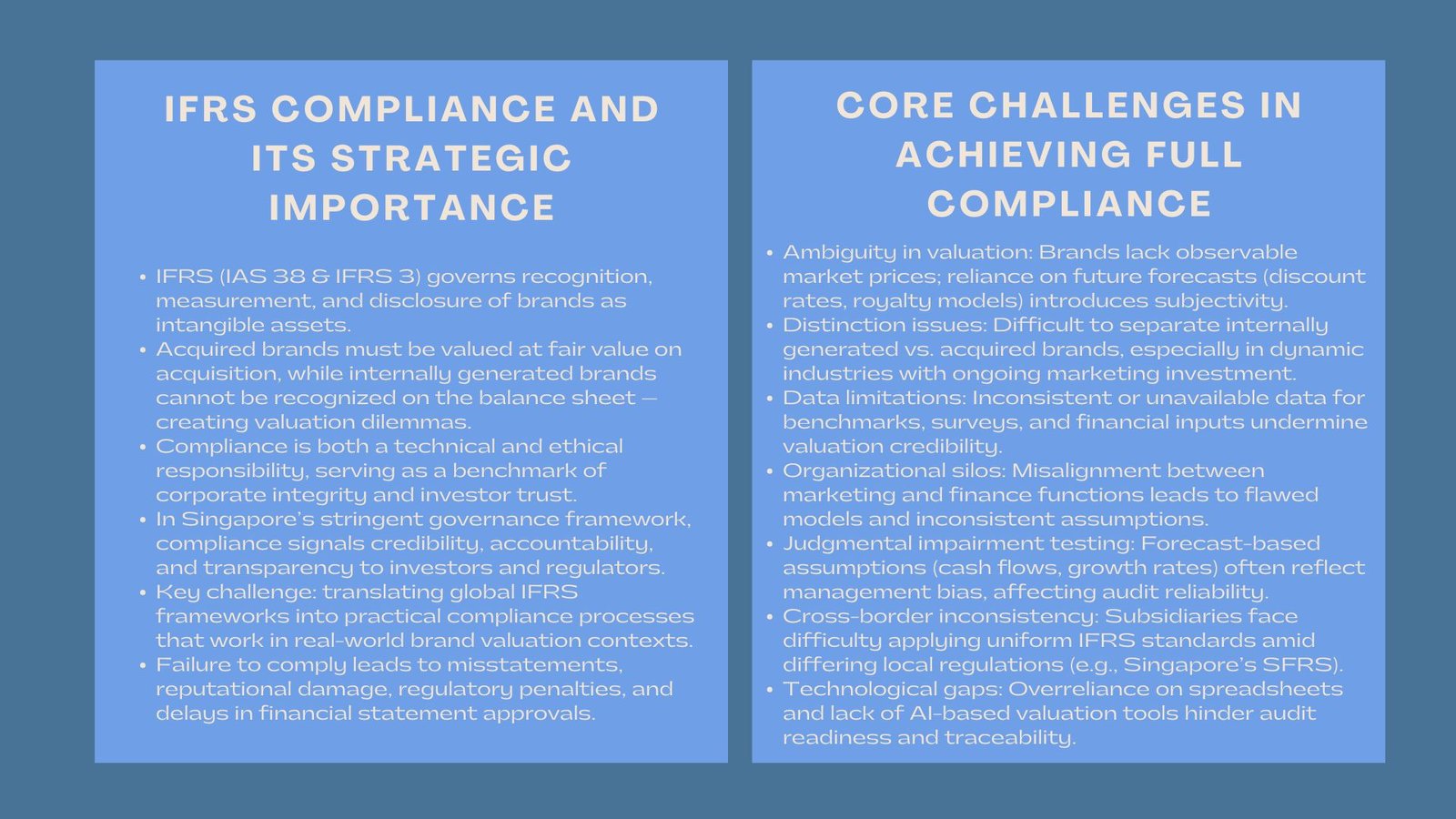

IFRS is an international reporting model of financial reporting that attempts to harmonize the financial reporting of firms. B brands are classified under intangible assets under IFRS, and it is mainly subject to IAS 38 (Intangible Assets) and IFRS 3 (Business Combinations). These standards provide provisions on recognition, amortization, impairment test and disclosure.

In the case of brands obtained by mergers and acquisitions, the valuation needs to be executed at the fair value, on the date of acquisition. Nevertheless, with internally generated brands, IFRS does not allow recognition in the balance sheet. This is an inherent difference that continually presents marketing and financial practitioners with dilemmas on how to align brand performance with accounting value.

1.2 The significance of Compliance.

Compliance is not just a technical feature that must be done, but it is also a test of corporate integrity. Failure to comply may result in material misstatements, reputational risk and fines by regulators. In Singapore, where accounting and auditing is highly harmonized with the international standards, compliance is a fundamental measure of the quality of governance and reliability by the investors.

2. Key Difficulties in Achieving Full IFRS Brand Valuation Compliance

2.1 Ambiguity in Valuing Intangible Assets

One of the foremost challenges in IFRS brand valuation compliance is the inherent ambiguity in valuing brands. Brands unlike tangible assets lack physical presence and an observable price on the market. Their value is based on the customer loyalty, brand strength and positioning with the competitors- all of which are subjective and variable.

The relief-from-royalty approach or excess earnings approach are some of the approaches that valuation professionals use but all approximations are made on future streams of revenue and discount rates and future growth. Any slight differences in these assumptions can drastically change the reported values and so adherence and consistency becomes a challenge over the reporting periods.

2.2. Inability to differentiate Between Internally Generated and Acquired Brands.

The IFRS makes companies differentiate between bought and own-created brands. In reality, though, such a distinction is not always as obvious as that. It is possible that a brand has been developed internally and then enhanced by purchasing or strategic alliances. The awarding of brand value as a recognized portion of the company brand value is regularly a question of judgment that an auditor can question concerning IFRS 3.

This difference is a persistent challenge to multinational firms, especially those in the fast-moving consumer goods where brand equity is constantly changing by making marketing investments and innovations.

3. Data and Measurement Challenges

3.1 Limited Access to Reliable Data

Reliable, verifiable data is the cornerstone of accurate brand valuation. However, companies often struggle to obtain consistent financial and non-financial data to support valuation assumptions. Market research, customer perception surveys, and royalty rate benchmarks may not be readily available or standardized.

In Singapore’s financial reporting environment, where brand reporting standards Singapore emphasize data-driven substantiation, the absence of reliable evidence can lead to disputes between management and auditors. This means that during the audit process, valuations can be questioned or re-examined which postpones the approval of financial statements.

3.2 Marketing and Finance functions are to be integrated

Brand valuation involves both marketing specialists (who can comprehend customer behavior and brand performance) and finance departments (who can decipher IFRS standards). Nonetheless, such departments usually work in silos, which creates the problem of miscommunication or poor valuation models. Compliance therefore necessitates cultural as well as structural alignment something many organization struggle to do uniformly.

4. Judgment and Interpretation in IFRS Application.

The subjectivity of impairment testing is based on the fact that accounting information is not reported in a standardized manner.<|human|>4.1 Testing of impairment- subjectivity

4.1 impairment testing is subjective because accounting information is not standardized.

IFRS requires testing of impairment of brands that have indefinite useful life on annual basis. Nonetheless, the process is heavily reliant on the decision of the management concerning the cash flow forecasts, discount rates, and long-term growth assumption. The subjectivity of these variables per se leaves the possibility of biasness, both deliberate or accidental.

The use of inconsistencies in the application of these assumptions is a recurrent finding in auditors in Singapore particularly where the market conditions are volatile. Excessively optimistic forecasts can result in the realization of impairment losses only too late whereas conservative ones can misrepresent brand value- a factor that undermines the role of IFRS.

4.2 Interjurisdictional inconsistencies.

In the case of multinational corporations, it is another complexity to provide uniformity in compliance in subsidiaries. Despite the intended international consistency of IFRS, local performance, taxation regulations and interpretation may cause inconsistency. Consolidation and group reporting is a major challenge because Singapore is very rigorous in embracing international norms that may not be that prescriptive when compared to other regions.

5. Technology and Analysis constraints.

5.1 Absence of sophisticated tools of valuation.

Notwithstanding the fact that technology is changing most of the facets of financial management, the use of AI-based valuation analytics is not even. The usage of spreadsheets and manual calculations is still common in many organizations which can be easily subjected to human error and can not be audited. Compliance documentation is hard to achieve without integrated systems up to the standards of the IFRS audit.

5.2 Emerging Role of Automation and Audit Preparedness.

State of the art valuation platforms have the capability to automatically record assumptions, audit trail revisions and give audit-ready reports. Nonetheless, they involve a huge investment and training to implement. Smaller companies or subsidiaries might not be capable of acquiring such systems, which increases the compliance gap between large and small multinational companies.

6. Cultural and Organizational Resistance to Compliance.

6.1 There is a weakness of lack of awareness and professionalism.

Meeting compliance does not only rely on the technical but also on human insight. Most marketing managers do not understand the IFRS principles and the financial personnel might not understand the performance of the brand. This gap in knowledge can only be addressed through specific training, interdisciplinary communication, and lifelong learning.

6.2 Resistance to Transparency

Some organizations have also internally resisted the disclosure of detailed valuation methodologies, believing that this information could expose the organization in terms of its strategies or be exposed to external review. When it comes to IFRS, however, transparency and justification of key assumptions are required. The inability to make such disclosure can be viewed as non-compliance or as a sign of poor internal governance.

7. Case Insights: Singapore Attitude towards Brand Reporting Compliance.

The Singapore Financial Reporting Standards (SFRS) is enforced by the Accounting Standards Council, Singapore, to enforce the IFRS-aligned standards in the country. Although similarity is high, audit quality and accountability are also the focus of the local regulators. The problem that many companies are having is how to reconcile the group-wide IFRS policies with SFRS implementation, especially on the level of disclosure and the documentation of its disclosures.

An example here would be multinational consumer goods companies that are based in Singapore. Some have had audit enquiries on their brand impairment models with the auditors doubting the soundness of assumptions. This shows that even advanced organizations face challenges when trying to achieve international and local compliance requirements.

8. Plans to beat the troubles of Compliance.

8.1 Empowering Cross-Functional Cooperation.

The development of a single system that will unify brand valuation and incorporate financial and marketing information assists in minimizing discrepancies. Algorithms can be used to check the assumptions made by joint review committees made up of experts in the fields of finance, marketing, and risk management to both fit with the IFRS and commercial facts.

8.2 Technology-Enabled Reporting Tools Implementation.

Valuation software and data visualization tools allow investors to increase the level of transparency, automate audit documentation, and be prepared to comply. These tools are able to incorporate external data sources, recreate various valuation situations, and produce reports according to the requirements of the IFRS disclosure.

8.3 Ongoing Training and Governance Supervision.

Compliance culture needs to be engrained through continuous education. The application of changing standards requires staff to be equipped with the knowledge through regular workshops, briefings on implementing the changes in the standards and simulating audits. Board-level accountability and the perpetual improvement.

Conclusion

Implementation of full compliance in brand reporting under IFRS is a continuous process, and not a one time event. The intricacy of valuation of intangible assets, as well as the dynamic character of the markets, implies that the most hard-working organizations encounter the same issues time and again. Non-compliance, however, can be tackled by examining the fundamental factors behind non-compliance, and companies could develop vigorous structures that increase transparency and credibility.

Conclusively, to excel in the IFRS brand valuation compliance, technical compliance is not enough and the stakeholders must ensure that their strategic alignment, technical innovation, and commitment to continuous improvement are in place. Firms using this mindset in Singapore and elsewhere will not only pass brand reporting standards Singapore but also gain investor trust and achieve sustainable financial performance in a world where disclosures are getting very popular.