Accounting Compliance for Digital Marketing Assets

As businesses accelerate their digital transformation, marketing activities increasingly rely on assets that exist almost entirely within digital ecosystems. From social media content, video campaigns, influencer partnerships, SEO assets, branded digital platforms, analytics software, and user-generated content initiatives, digital marketing now represents a substantial component of brand building and revenue generation. Despite their strategic importance, these digital marketing assets pose unique accounting challenges due to their intangible nature, rapid depreciation, multi-channel usage, and complex ownership rights. As regulatory expectations tighten and auditors demand greater clarity, organizations must ensure that the recognition, measurement, and reporting of these assets align with international accounting frameworks. This has intensified the critical role of digital marketing asset IFRS compliance, requiring companies to interpret IFRS principles in modern digital contexts. In parallel, regional markets such as Singapore—home to sophisticated regulatory standards and strong corporate governance—expect transparent and accurate reporting through specialised practices in brand asset accounting Singapore. Together, these requirements shape a new era of financial discipline, compelling companies to elevate how digital marketing assets are classified, valued, amortized, and disclosed across corporate reporting cycles.

Understanding the Nature of Digital Marketing Assets

The Rising Complexity of Digitally Driven Brand Investment

Digital marketing has expanded far beyond traditional online advertising. Companies now deploy multi-layered digital ecosystems involving community platforms, branded content libraries, algorithm-driven targeting tools, e-commerce integrations, and long-term digital brand experiences. These assets often involve outsourced production, licensing rights, third-party collaborations, and proprietary technology stacks. The complexity arises because digital marketing assets are fluid, continuously updated, rapidly consumed, and often intertwined with platforms that the company does not own. This dynamic environment forces companies to delineate between what qualifies as an intangible asset under IFRS and what remains a period expense. Understanding this distinction is essential for ensuring compliance and avoiding audit disputes, especially for organizations navigating digital brand asset accounting IFRS Singapore requirements.

Differentiating Capitalizable Digital Assets From Operating Expenditures

One of the most challenging issues is determining whether a digital marketing asset creates long-term economic benefit or merely serves as a short-lived promotional expense. Websites, mobile applications, brand films, evergreen campaign materials, and specialized visual assets may meet the criteria for capitalization—provided they generate future economic inflows and the company maintains control over the asset. In contrast, programmatic ads, influencer posts, and real-time social content typically do not. The criteria under IFRS, particularly IAS 38, require strict adherence to conditions such as identifiability, control, and the expectation of future economic benefit. Companies must carefully evaluate each digital initiative to classify it correctly and maintain consistent accounting treatments across reporting periods.

Applying IFRS to Digital Marketing Assets in a Modern Context

Interpreting IAS 38 for Digital Assets With Short Life Cycles

IAS 38 governs intangible assets, but its principles were drafted long before digital marketing ecosystems became as complex as they are today. As a result, companies must interpret IAS 38’s core concepts—from identifiability and control to measurable cost—in light of rapidly created and consumed digital content. Many digital assets have shorter useful lives due to viral consumption, platform algorithm shifts, and fast-changing creative trends. Companies must therefore develop robust frameworks to estimate useful life, amortization patterns, and impairment triggers that align with the reality of digital consumption habits. Failing to adjust these assumptions risks misalignment between accounting figures and economic performance.

Determining Control in Partnership-Driven Digital Environments

Control is a critical IFRS criterion. In digital marketing, however, control becomes blurred when assets are hosted on platforms owned by third parties such as Meta, Google, TikTok, or e-commerce marketplaces. The company may own the creative output but not control the platform through which it delivers value. Companies must examine whether they have exclusive rights to use, modify, or monetize the asset to determine capitalization eligibility. This assessment becomes crucial for long-term digital assets such as brand-owned content hubs, interactive brand tools, and proprietary software-driven marketing systems.

Assessing Future Economic Benefits From Digital Campaigns

Under IFRS, future economic benefits must be probable and measurable. Yet digital marketing outcomes often involve indirect returns such as engagement, reach, sentiment, and long-term brand lift. Companies face challenges in quantifying how a digital asset contributes to revenue. Some companies use proxy indicators such as conversion rates, customer lifetime value improvements, repeat purchase frequency, and brand equity enhancement. While these proxies support capitalization decisions, they must be applied consistently and documented thoroughly to meet IFRS audit requirements.

Singapore’s Framework for Brand and Digital Asset Accounting

High Governance Standards Driving Stronger Compliance Requirements

Singapore is known for its robust regulatory environment, investor-friendly transparency standards, and commitment to high-quality corporate reporting. For companies operating in Singapore, brand asset accounting Singapore demands stricter attention to valuation and recognition processes. Regulators, boards, and audit committees expect coherent frameworks that reflect the economic substance of digital brand investments. As brands depend increasingly on digital channels to reach local and regional audiences, Singaporean companies must ensure that their accounting treatments align not only with IFRS but also with best practices adopted by the Singapore Accounting Standards Council.

Navigating Regional Interpretations of Global IFRS Principles

Although Singapore adopts IFRS standards closely through the Singapore Financial Reporting Standards (SFRS), regional interpretation of digital marketing assets may vary. Singapore’s emphasis on prudence, documentation, and risk mitigation influences how intangible assets are recognized. Companies must therefore align their accounting policies with Singapore’s financial reporting culture, which requires detailed justification for capitalization decisions and heightened scrutiny of future benefit assumptions. This ensures that valuations and intangible asset balances remain credible and defensible during audits.

Addressing Tax, Licensing, and IP Considerations for Digital Assets

Singapore’s tax framework interacts with digital marketing assets in ways that influence their accounting treatment. For example, capitalized intangible assets may be subject to specific tax allowances, while certain digital advertising costs remain non-capitalizable. Licensing arrangements, cross-border intellectual property rights, outsourced creative production, and digital asset ownership structures must all be accounted for consistently. Companies must align their accounting, tax, and IP management systems to ensure that digital marketing assets are recognized and amortized in accordance with local tax laws and IFRS-based reporting standards.

Valuation and Impairment Considerations for Digital Marketing Assets

Establishing Reliable Valuation Techniques for Digital Intangible Assets

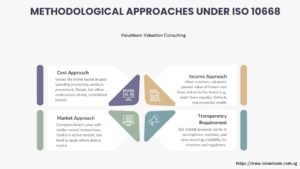

Digital marketing assets rarely come with traditional valuation comparables, making their fair value assessment more complex. Because many digital assets contribute indirectly to brand-building, companies rely on valuation approaches such as relief-from-royalty, replacement cost, or multi-period cash-flow models adjusted for digital engagement metrics. While these approaches may not perfectly capture digital intangibles, they provide methodological rigor that auditors expect when evaluating capitalization choices. This valuation discipline is especially critical in the Singapore context, where brand assets often undergo detailed audit inspection.

Impairment Testing Under IAS 36 for Rapidly Evolving Digital Assets

IAS 36 requires companies to assess whether intangible assets have become impaired. Digital marketing assets face heightened impairment risk due to rapidly shifting consumer habits, technological changes, and competitive dynamics. Assets that were once high-performing may lose relevance if platform algorithms change or consumer attention shifts to new formats. Companies must integrate digital performance metrics—such as traffic decay, engagement decline, or tech obsolescence—into impairment testing. This ensures timely recognition of losses and prevents overstated asset balances.

Monitoring Useful Life and Amortization in Digital Environments

Unlike traditional intangible assets, digital marketing assets often have unpredictable or extremely short useful lives. Companies must estimate amortization schedules that reflect actual consumption and technological decay. Some digital assets may require accelerated amortization due to short-term relevance, while others—such as long-term brand films or evergreen content hubs—may sustain economic benefits for multiple years. Accurate amortization improves reporting clarity and ensures transparency in financial statements.

Governance, Risk, and Internal Controls for Digital Marketing Assets

Developing Internal Frameworks for Digital Asset Recognition and Review

Organizations must establish internal control systems that guide how digital marketing assets are evaluated, approved, recorded, and reviewed. These systems define which digital deliverables may be capitalized, who approves capitalization decisions, how useful life estimates are determined, and how impairments are monitored. Strong internal governance ensures consistent application of IFRS rules across departments.

Ensuring Transparent Collaboration Between Marketing and Finance Teams

Digital marketing teams often operate independently from finance, creating gaps in understanding around asset identification, cost structures, and ownership rights. To ensure compliance, marketing must document asset creation processes, campaign objectives, usage patterns, and platform rights. Finance teams, in turn, must interpret this documentation through the lens of IFRS. Close collaboration increases transparency and ensures that accounting treatments accurately reflect underlying economic realities.

Managing Digital Asset Risks Including Obsolescence and Security

Digital assets carry unique risks: loss of relevance due to social trends, technological failure, platform discontinuation, or cybersecurity breaches. Companies must integrate risk assessment into digital asset governance. Failure to assess these risks may lead to overstated asset values, unrecognized impairment, or compliance gaps. Robust risk governance ensures that digital assets remain accurately measured and protected across their lifecycle.

Conclusion to Accounting Compliance for Digital Marketing Assets

Accounting for digital marketing assets is becoming a critical requirement as companies shift toward digital-first brand-building strategies. Ensuring compliance with digital marketing asset IFRS guidelines is essential for recognizing, measuring, and reporting intangible digital assets accurately. In markets such as Singapore, where reporting discipline and corporate governance are highly prioritized, developing strong frameworks for brand asset accounting Singapore is indispensable. As digital marketing continues to evolve, companies must refine their accounting policies, valuation techniques, impairment assessments, and governance structures. Through thoughtful and rigorous compliance practices, organizations can create transparency, strengthen financial credibility, and support long-term brand and business performance.