Implementing Brand Valuation for Licensing Deals: IFRS-Aligned Approaches for Technology Brands

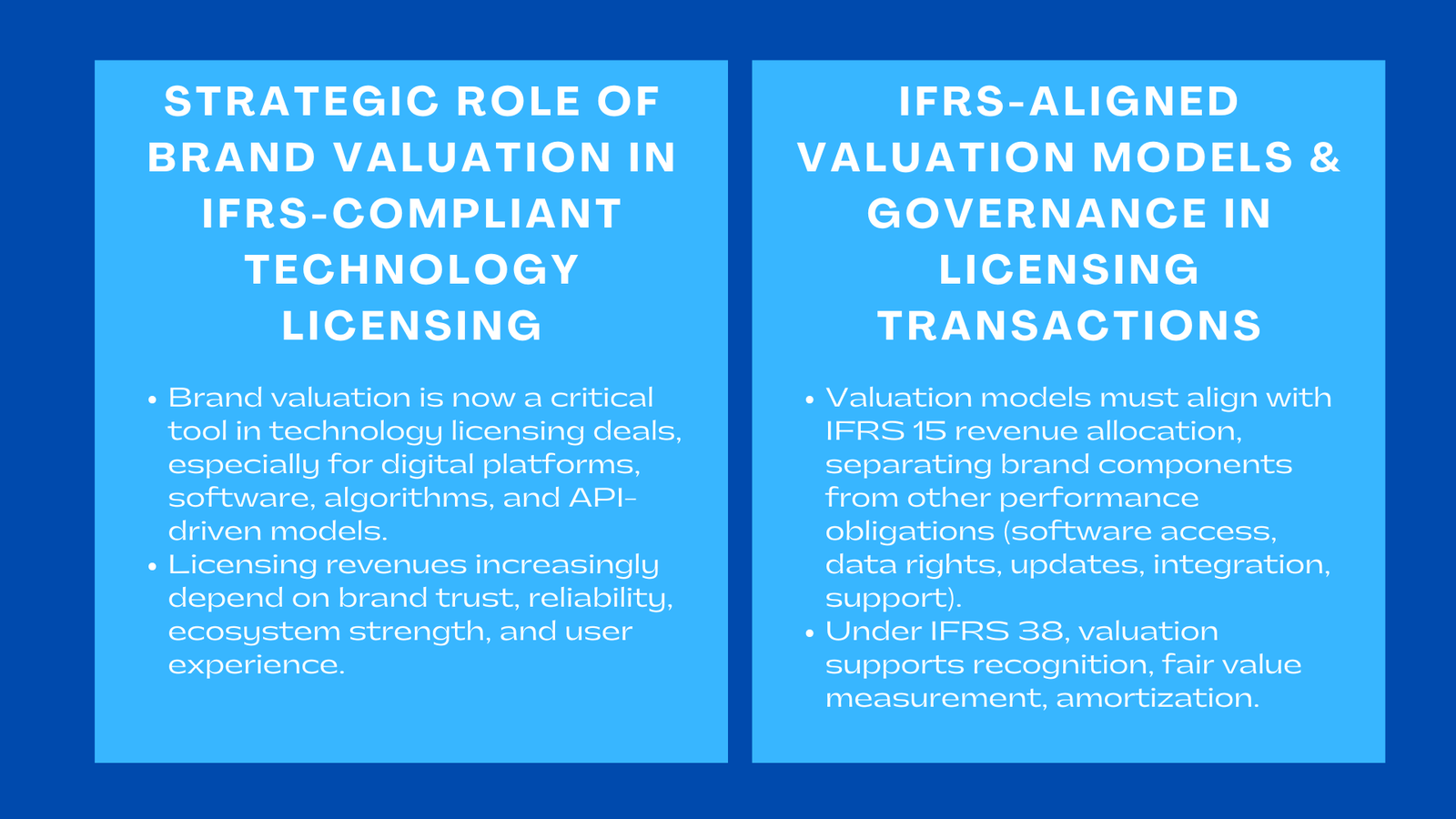

The brand valuation has now been a key strategic instrument of licensing arrangements by technology companies, particularly amid the growth of digital ecosystems and the increased importance of intellectual property assets in the revenue stream. In the case of software platforms, products based on algorithm and API-driven business models, licensing activity is used to define financial results and investor anticipations more and more. However the reporting of such arrangements in terms of finance is reported under strict International Financial Reporting Standards (IFRS) which stipulates that companies should make valuation methodologies compliant to accounting principle to make disclosures transparent and defensible. This paper discusses how brand valuation may be conducted in a systematic way to assist in IFRS compliant reporting in technology licensing transactions, providing insights similar to understanding IFRS 13 fair value measurement Singapore, with a focus on the practical needs, accounting considerations, and administrative structures to enable consistency and credibility.

1. Valuation of Brands as a Prerequisite in IFRS-Compliant licensing.

1.1 The Importance of Brand to Technology licensing Transactions.

Trust, reliability, user experience, and ecosystem influence are a very important source of value to technology brands. In the case of licensing software, data, or APIs, the perceived quality and credibility of the brand have a significant impact on price, adoption and terms of the contract. This renders the brand valuation, not only a marketing exercise, but a financial necessity. Nevertheless, IFRS stipulates that the valuation of identifiable intangible assets, economical assumptions that are supportable and reliable measurements be used in the financial statements. Thus, at the very beginning, the accounting standards should be closely combined with valuation to guarantee that the transactions of licensing will be documented accurately and in a way that meets the regulatory requirements.

1.2 IFRS Requirements that have fuelled Valuation Discipline.

The basis of revenue recognition under IFRS 15 and the intangible assets under IFRS 38 is the tech licensing arrangements. These standards determine the way companies determine the prices of transactions, the performance requirements, and quantifying the value of licensed rights. Intense valuation assists in deciding whether the brand-related premiums within a licensing contract ought to be viewed as revenues, identified as an intangible asset, or be apportioned among various elements of the contract. This is why the valuation should be recorded in such a way that it will pass an audit examination and comply with the IFRS measurement principles, such as the presence of the proper discount rates, sustainable cash flow projections, and justifiable assumptions of allocating them.

2. Incorporating Valuation Models in the Process of Licensing Accounting.

2.1 Matching Valuation inputs with IFRS 15 Revenue Allocation.

Under the IFRS 15, licensing transactions necessitate entities to assign contract consideration to every separate performance need. The obligations in technology licensing can be software access, updates, data rights, branding rights, platform integration and customer support. The stand alone value of the brand related components will be determined by a valuation model which will guarantee proper allocation. Indicatively, when a technology platform charges a high price due to good brand reputation, valuation can measure the brand-related component of the contract and justify its treatment under the IFRS 15. This will stop misappropriation of revenue and enhance reliability of financial reporting.

2.2 Recognizing Intangible Assets Supported by IFRS 38.

In other licensing deals a technology company can purchase branding rights or licence a brand as part of a larger intangible transfer. The new IFRS 38 ensures that the intangible assets are identifiable and controlled by the organization and that they produce future economic benefits. Structured valuation determines whether a brand right has reached recognition thresholds as well as assessing their fair value towards capitalization. Moreover, valuation models will be used to have the amortization schedules and impairment testing, which should be aligned to the IFRS to provide quality reporting throughout the useful life of the asset. Brand valuation is a support structure of intangible balance sheet treatment when it is undertaken systematically.

3. Overcoming the obstacles associated with IFRS-Related Licensing Valuation.

3.1 Separating Brand Value and Technology Functionality.

Among the greatest complications in technology licensing is the distinction between brand-driven value and functional intellectual property value. The valuation as required by IFRS is needed to isolate identifiable elements and prevent the overstatement of intangible assets. As an illustration, the revenue of premium licensing can be based on the part of high-quality engineering, part on brand recognition and part on the network effects of the user base. Valuation should break down such drivers such that accounting allocation is precise. This disaggregation also plays a vital role in the audit of the regulators and auditors who analyze the compliance of the identified value with economic reality and the definitions of the IFRS.

3.2 How to cope with the Future Unpredictability of Tech Ecosystems.

Technology markets are changing very fast and this presents uncertainty in the cash flow projections applied in valuation models. According to IFRS, the support, documentation, and consistency of assumptions must be in line with external evidence. Consequently, technology firms have to show that the basis of license revenue projections, particularly where the brand premium is involved, is based on realistic market adoption curves, customer churn models and positioning. In their absence, valuations can be questioned on the basis of speculative or optimistic assumptions, and put companies at a compliance risk and restatement loyalty.

4. Enhancing Governance of IFRS-Aligned Valuation at licensing.

4.1 The fourth principle is to have Standard Valuation Policies.

To successfully incorporate the brand valuation into the IFRS accounting, technology firms need to come up with internal rules on how valuation is acceptable, documentation frameworks, review of assumptions, and cross-functional roles. Standardization safeguards against irregular practices between business units and assures that every licensing dealings irrespective of geographical location or products covered are backed by justifiable valuation evidence. These policies are also consistent in the valuation outputs with the functions of finance, legal and compliance, to create consistency in the audit cycles.

4.2 Improving the work of the Finance, Legal, and Product Teams.

The transactions that are often involved in the process of licensing are the product management, engineering, marketing and finance departments. To be IFRS-compliant, the input assumptions should be based on the realities of operations, including the terms of the contracts, the features of platforms, metrics used by users, and their competitive positioning. Interdepartmental cooperation will guarantee that the money models reflect the actual economic guts of the structure. This integration minimizes the risk of compliance, and it enhances the credibility of disclosures to investors and regulating bodies.

5. Application of Selected Keywords within IFRS-Linked Contexts

Technology companies engaged in licensing activities increasingly rely on frameworks such as Brand licensing valuation guide to strengthen the defensibility of valuation methodologies used in financial reporting. At the same time, audit teams and compliance officers emphasize adherence to Licensing compliance IFRS, particularly when licensing arrangements include complex intangible asset components or multi-element performance obligations. Such considerations have become the focal point in the management of licensing-based business models, which lead to internal policies and affect investor-disclosures.

Conclusion to Implementing Brand Valuation for Licensing Deals IFRS-Aligned Approaches for Technology Brands

It has become necessary to incorporate brand valuation into IFRS reporting of transactions involving licensing of technology to ensure transparency, accuracy, and strategic credibility. With the growth of digital ecosystems, and the increase in intangible assets becoming leading contributors to enterprise value, technology firms need to establish that licensing arrangements are backed up by valuation models that comply with IFRS 15 and IFRS 38. With the introduction of an organized policy, the improvement of cross-functional cooperation, and basing the valuation assumptions on the reality of business operations, businesses could raise the level of compliance and mirror the value of the brand in the financial statements. Such a disciplined practice is not only making the regulatory conduct defensive, but it also enhances the confidence of investors in the long-term viability of the licensing-based business model.