Accounting and Compliance for Hospitality Brands: Mastering IFRS in a Complex Service Environment

The complexity of accounting and compliance requirements in the hospitality industry continues to increase due to international opera of operation, multilocation revenue structure and increased dependence on intangible assets to create competitive advantage. Hotels, resorts and hospitality groups rely significantly on the power of its brand, delivery of its guest experiences and service innovation but these capabilities should be correctly reflected in the International Financial Reporting Standards (IFRS). With increased pressure on global investors, regulators, and operators to have transparent reporting, the hospitality brands are under increased scrutiny in terms of how the brand assets are valued, measured and disclosed. It is now necessary to understand the accounting and compliance realities of this industry that have evolved to be central to financial leadership especially as brand equity turns out to be a fundamental source of long-term enterprise value, similar to the precision required in how to do valuation of an accounting business Singapore when assessing intangible-driven enterprises.

1. The Accounting Situation of Hospitality Brands.

1.1 The Different Character of Hospitality Brand Assets.

Hospitality brands create value by creating consistency in the services, loyalty programs, franchise networks, and reputation- however, these resources are intangible and are hard to measure within the traditional accounting frameworks. The under IFRS it should be recognized based on demonstrable future economic benefits and reliability which in turn is difficult to achieve with the intangibles of the hospitality brand. As an example, repeat bookings are based on the guest loyalty, and customer relationship cannot be monetized unless bought. This places hotels in a dilemma at all times, the strength of the brand obviously has an effect on the enterprise value, yet IFRS constrains what can be reflected on the balance sheet. This renders responsible accounting judgment and systematic valuation framework.

1.2 Multi-Brand, Multi-Location Complications

The majority of hospitality corporations in the world have several brands in various regions under different ownership structures; owned, managed, franchised and asset-light models. Each model has its distinct implication on revenue recognition, contract assets, treatment of intangibles and testing of impairments. As an illustration, royalty income associated with the usage of brands may be produced as a result of franchise agreements, and the terms of such contracts will have to be carefully assessed according to IFRS 15. In the meantime, management contracts are performance-linked with delivery of operations and satisfaction of the guests. Such multi-levels of complexity require exact accounting governance to make sure that it follows the rules, as well as brand economics to mirror faithfully.

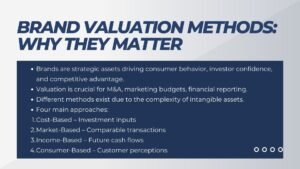

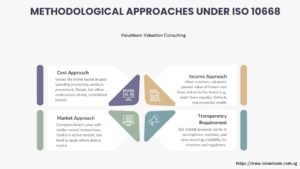

2. Brand Valuation under the IFRS: What Hospitality companies need to know.

2.1 The IFRS Framework of Recognition of Brand Intangibles.

Strategic or investor often face purposes of brand valuations are a common direction of hospitality brands. Nonetheless, brand recognition is only permitted under IFRS in special circumstances- mostly in a business combination under IFRS 3. Even those internally created brands which may be international are not to be capitalized. This limitation influences the way in which hotel chains are reporting brand equity, which tends to under-represent the strategic value of brand equity in financial reports. As a result, CFOs should ensure that management and internal statistical valuations are not mixed with IFRS-compliant valuations to avoid misunderstanding by investors or regulators when reporting the results to the statutory report.

2.2 Requirements of Impairment Testing Brand Intangibles.

Hospitality brand intangibles should be impaired annually when identified under IAS 36. Such tests may be especially sensitive towards hotels since the performance of the brand is closely related to the conditions of the market, customer attitudes and occupancy rates. Other impairment reviews may be caused by such events as economic downturns, travelling delays, or repositioning of the brand. The difficulty is in the ability to predict a cash flow of the hospitality CGUs (Cash Gen Units) that often involve a number of interdependent drivers of revenue. The strength of the valuation model and management assumptions are conclusive in proving that IFRS is being followed.

3. Practical Problems that are Pushing the Need of a Strong Accounting Governance.

3.1 The first one concerns the excessive reliance on forecasting in a dynamic industry.

Hospitality brands are being competed in a dynamic environment due to seasonality, competition, global tourism patterns and geopolitical risks. It is hence very difficult to make predictions on the revenues to be used in impairment testing, or intangible valuation. Financial projections must be updated on a regular basis whether it is the expected occupancy or the average daily rates, or the costs of acquiring guests. Low predictive validity puts the brands at risk of compliance failures, audit disputes, or an outcome of misaligned valuation. This would render rigorous modelling and scenario planning imperative elements of financial governance.

3.2 Duplicative Intangibles Customer Experience, Loyalty and Brand Value.

The other complication is the dependence of the hospitality industry on intangibles based on experience, which interplay with brand value. The aspects like guest experience design, service culture, and the economics of loyalty program offer value to the creation. However, under IFRS, every intangible should be identifiable and measurable, and not always easy. This creates the dilemma of practical accounting: is brand, customer relationship, or loyalty program to be allocated its value? The solution will have an impact on the amortization periods, impairment triggers, and disclosure requirements which will directly impact the regulatory compliance.

4. Enhancing Compliance with Strategic Accounting Practices.

4.1 Establishing a Strong Policy System.

It is necessary that hospitality groups should come up with internal accounting policies, which will translate the IFRS guidance across brands and areas. These policies will have to determine how the company will categorize intangible assets, how they will carry out impairment testing, how they will estimate contract revenue under the IFRS 15, and how they approach the purchased brand intangibles. Clear structure helps to minimize risk of interpretation, to make things globally consistent and offer auditors clear documentation.

4.2 Improving Interdepartmental Co-operation.

Compliance is not a totally accounting role, but it relies on the knowledge of marketing, operations, development, and legal departments. As an illustration, it is critical to comprehend the concept of branding, royalty assignments, and asset management model to establish how to treat them under accounting. By integrating the departments, the hotels will be able to generate the financial statements that can be qualified as appropriate to the business model and might resist the regulatory audit.

5. The Technology in Enhancing Brand Accounting and Compliance.

5.1 Centralized Financial Reporting Systems

A large number of hotel chains continue to use decentralized financial reporting systems because of the property-level independence and franchise systems. With centralized systems, reporting is done in a standardized way, automated consolidation and uniform treatment of intangible assets is presented. Automation eliminates mistakes, accelerates reporting and improves compliance records.

5.2. Advanced Forecasting Analytics.

The use of modern analytics can enhance the accuracy of the forecasts made on impairment testing and intangible valuation. The predictive models that use the booking patterns, market trends, and competitive benchmarking have more credible inputs as compared to the manual methods. Better understanding increases the defensibility of the IFRS judgments and enhances compliance and investor trust.

- Applying Keywords Naturally Within Context

In practice, accounting teams in the hospitality sector increasingly reference specialized frameworks such as Hospitality brand accounting IFRS to ensure consistency across properties, franchises, and merged entities. At the same time, compliance teams are strengthening oversight by implementing more structured policies that support Brand compliance in hotels, especially as regulators emphasize transparent reporting and robust intangible asset measurement. The themes are currently influencing financial strategy throughout the hospitality sector brands, as they make the reporting quality to improve, and the financial statements to reflect the economic realities of the industry.

Conclusion to Accounting and Compliance for Hospitality Brands Mastering IFRS in a Complex Service Environment

Hospitality brands accounting and compliance under IFRS is turning out to become a strategic competence and not necessarily a regulatory mandate. As brand equity and loyalty ecosystem, and guest experience are the pillars of the competitive advantage, hotel groups should base their financial reporting on the real drivers of business. The complexity of the hospitality industry operations, such as contract arrangements, multi-brand portfolio and intensive business model that are mostly intangible requires stringent accounting governance that is aided by technology, analytics and cross functional integration. Hospitality brands can communicate their interests and attract better valuations and long-term stability in the ever-competitive international market by becoming more compliant and having financial reporting at the center of their operations.