Accounting Treatment for Franchise Brands

Franchise brands represent a unique category of intangible assets that intertwine legal, operational, and financial complexities. Unlike wholly owned brands, franchise brands involve a network of franchisors and franchisees, sharing both benefits and responsibilities. Accounting for franchise brands requires adherence to International Financial Reporting Standards (IFRS), particularly IAS 38 for intangible assets and IFRS 15 for revenue recognition, to ensure accurate, transparent, and compliant financial reporting.

Proper accounting treatment is critical not only for regulatory compliance but also for strategic management. Accurately valuing franchise brands provides insights into market positioning, expansion potential, marketing investments, and licensing fees. In markets such as Singapore, where franchising is a growing sector in food and beverage, retail, and service industries, robust accounting practices strengthen investor confidence, support sustainable growth, and enhance brand credibility. Franchise brand accounting IFRS are more than contractual arrangements—they are strategic assets that influence long-term enterprise value, market perception, and competitive advantage.

Recognition of Franchise Brand Assets

Identifiability and Control

To recognize a franchise brand as an intangible asset under IFRS, the brand must satisfy two core criteria: identifiability and control. Identifiability ensures that the brand can be separated, transferred, or licensed independently from other business assets. Control requires that the franchisor has the legal or contractual right to derive economic benefits from the brand and restrict unauthorized use by others. In the context of brand strength and brand equity valuation in Singapore businesses, these criteria are essential to ensure that the recognized franchise brand accurately reflects its true market and financial value.

Franchisors typically retain ownership of trademarks, logos, service marks, and proprietary business processes. Licensing agreements outline operational standards, marketing obligations, quality assurance requirements, and royalty structures, reinforcing control. Documentation of these agreements is essential to demonstrate compliance with IFRS and to support accurate asset recognition. Without meeting these criteria, a franchise brand cannot be recorded as an asset, which may undervalue the company’s financial position and misrepresent its strategic capabilities.

Revenue Streams and Licensing Fees

Franchise brand value often derives from multiple revenue sources, including upfront franchise fees, ongoing royalties, marketing contributions, and support services. Accurate accounting requires distinguishing between revenue types and applying IFRS 15 guidelines for revenue recognition.

For example, an initial franchise fee might be recognized over the duration of the contract, reflecting ongoing support obligations. Royalties based on sales performance may be recognized monthly or quarterly, depending on fulfillment of performance obligations. Marketing contributions and shared promotional expenditures should be carefully attributed to ensure they accurately reflect the brand’s economic benefit. Correctly distinguishing these revenue streams provides clarity, strengthens auditability, and ensures financial statements accurately reflect brand-related income.

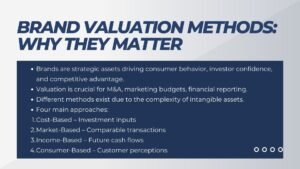

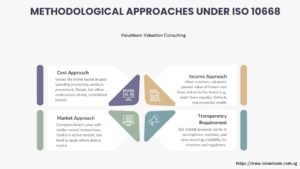

Valuation Methodologies for Franchise Brands

Income Approach

The Income Approach estimates the present value of expected future cash flows generated by franchise operations. This includes revenue from franchise fees, royalties, and projected market growth.

For instance, a fast-food franchisor in Singapore with 50 franchise locations might forecast royalties and fees over a 10-year period, discounting future cash flows to reflect risk and time value. Assumptions include market expansion, competitor activity, operational risks, and brand reputation. This approach provides a defensible valuation methodology for investors and auditors, ensuring that financial reporting reflects realistic expectations of economic benefits.

Market Approach

The Market Approach benchmarks the franchise brand value against comparable transactions, such as historical franchise sales, licensing agreements, or acquisitions of similar brands. While obtaining comparable data may be challenging for specialized or unique franchise brands, this approach provides external validation for internally derived valuations.

For example, a boutique retail franchisor can compare its valuation with similar regional franchise agreements or recent acquisitions to ensure the internal estimates are reasonable. This method strengthens investor confidence and provides a market-based perspective on the brand’s worth.

Cost Approach

The Cost Approach estimates the cost required to develop, maintain, or replicate the franchise brand. This includes expenses related to marketing campaigns, staff training, operational support, and legal protection of intellectual property.

For emerging or early-stage franchises with limited revenue history, the Cost Approach provides a conservative measure of the brand’s minimum value. It also highlights the investment in brand-building and operational excellence, reinforcing the tangible contributions of intangible assets.

Amortization and Impairment Considerations

Finite Useful Life of Franchise Brands

Franchise brand assets typically have finite useful lives linked to franchise agreements or market relevance. Determining useful life requires assessing factors such as market trends, competitive pressures, consumer behavior, and technological innovations. Brands in rapidly evolving industries, such as tech-driven service franchises, may face shorter useful lives due to obsolescence or changing customer preferences.

Regular Impairment Testing

Impairment testing ensures the carrying value of franchise brands does not exceed recoverable amounts. Companies must assess whether projected cash flows, royalty income, or market conditions justify current valuations. Documenting assumptions, including discount rates, projected revenues, and operational risks, enhances transparency, supports audit readiness, and provides investors with confidence in the reliability of financial statements.

Scenario Analysis and Sensitivity Testing

Franchisors should perform scenario analysis and sensitivity testing to evaluate the impact of changes in market conditions, competitor behavior, or regulatory frameworks. These tools help identify vulnerabilities in projected cash flows and inform proactive mitigation strategies. For instance, a sudden change in food safety regulations could affect operational costs and royalties, impacting brand value if not accounted for in scenario planning.

Reporting and Compliance Requirements

Transparent Financial Statements

Transparent reporting is critical for both compliance and strategic management. Financial statements should clearly describe the recognition, valuation methodology, amortization schedule, and impairment assessments of franchise brands. Such disclosures allow investors, auditors, and franchisees to understand how intangible assets contribute to enterprise value.

Cross-Functional Collaboration

Accounting for franchise brands requires integration across finance, legal, operations, and marketing departments. Finance teams ensure compliance with reporting standards, legal teams manage contracts and IP rights, operations teams provide insights into performance metrics, and marketing teams contribute data on brand development and network growth. Cross-functional collaboration ensures accurate reporting, reduces risks of misstatements, and supports governance best practices.

Audit Readiness and Documentation

Documenting valuation methods, revenue recognition policies, and impairment analyses is essential for audit readiness. Clear records demonstrate adherence to IFRS standards, facilitate due diligence by investors, and show that the franchise brand is actively managed as a strategic asset rather than a passive intangible entry.

Strategic Implications for Franchisors

Expansion Planning and Market Growth

Accurate franchise brand accounting informs strategic decisions, including market entry strategies, franchise fee structures, and marketing investments. Quantifying brand value enables franchisors to prioritize high-return initiatives, assess ROI, and expand networks sustainably while mitigating risk.

Mergers, Acquisitions, and Strategic Partnerships

Franchise brand valuation plays a crucial role in mergers, acquisitions, and strategic alliances. Documented brand value allows for better negotiation during acquisitions, licensing agreements, or partnerships, aligning expectations and reinforcing enterprise value.

Investor Confidence and Stakeholder Engagement

Transparent accounting and valuation practices enhance investor confidence by demonstrating that franchise networks are a managed, valuable component of corporate assets. Stakeholders—including franchisees, regulators, and banks—gain a clear understanding of the brand’s performance, resilience, and revenue potential, building trust and long-term strategic relationships.

Risk Management and Operational Resilience

Franchise brand valuation also supports risk management. By assessing potential revenue fluctuations, market changes, and operational risks, franchisors can implement strategies to mitigate negative impacts on brand equity. Regular revaluation ensures the organization responds proactively to changes, maintaining the brand’s financial and strategic relevance.

Case Study: Singapore F&B Franchise

A leading F&B franchisor in Singapore operates 60 franchise locations across Southeast Asia. The company implemented a comprehensive accounting framework for franchise brands, incorporating Income, Market, and Cost Approaches. Revenue projections included royalties, upfront franchise fees, and marketing contributions, with assumptions based on market growth, operational efficiency, and competitive landscape.

Scenario planning and sensitivity analysis accounted for changes in regulations, shifts in consumer behavior, and new market entrants. Cross-functional collaboration ensured accurate reporting of operational performance, marketing compliance, and IP protections. Transparent financial statements facilitated investor confidence, enabled regional expansion, and supported negotiations with franchisees and strategic partners. Continuous monitoring allowed the company to update assumptions, detect emerging risks, and maintain accurate brand valuation over time.

Conclusion to Accounting Treatment for Franchise Brands

Franchise brand accounting under IFRS is complex but strategically critical. Recognition, valuation, amortization, and reporting are not merely compliance requirements—they are essential for leveraging franchise brands as growth engines and strategic assets. Companies that implement structured methodologies, transparent reporting, and cross-functional collaboration can maximize the value of their franchise networks, protect intangible assets, and enhance long-term enterprise value.

Accurate accounting informs market expansion, marketing investments, royalty structures, mergers and acquisitions, and stakeholder communication. By regularly performing impairment testing, scenario planning, and sensitivity analysis, franchisors mitigate risk and maintain the resilience of brand equity. Transparent and detailed documentation supports audit readiness, reinforces investor confidence, and demonstrates governance excellence.

In highly competitive markets like Singapore, effective franchise brand accounting translates intangible assets into measurable financial and operational advantages. It empowers franchisors to strategically manage their networks, align business strategy with brand performance, and ensure sustainable, long-term growth. By treating franchise brands as dynamic, managed, and strategic assets, organizations can maximize revenue potential, strengthen stakeholder trust, and maintain a competitive edge. Ultimately, brand reporting for franchise accounting is not just about compliance—it is a framework for strategic value creation, operational excellence, and enterprise resilience.